Download presentation

Presentation is loading. Please wait.

1

Chapter 5 Financial instruments

2

SharesDerivatives & futures

3

Relevant standards IAS 32 IAS 39 IFRS 7 IFRS 9

4

Definitions Financial instruments Financial assets Financial liabilities Equity instruments

5

Recognition and de- recognition Recognition when the company becomes a party to the contractual provisions of the instrument, rather than when the contract is settled. (ie, derivatives)

.")

6

Recognition and de- recognition De-recognition Financial Assets (FA): -- the contractual rights to the cash flows expired, or -- substantial risks and the rewards of ownership of the financial asset has been transferred (eg sold).

: -- the contractual rights to the cash flows expired, or -- substantial risks and the rewards of ownership of the financial asset has been transferred (eg sold).")

7

Recognition and de- recognition Financial liabilities (FL): --when it is extinguished that is when the obligation is discharged, cancelled or expired

: --when it is extinguished that is when the obligation is discharged, cancelled or expired")

8

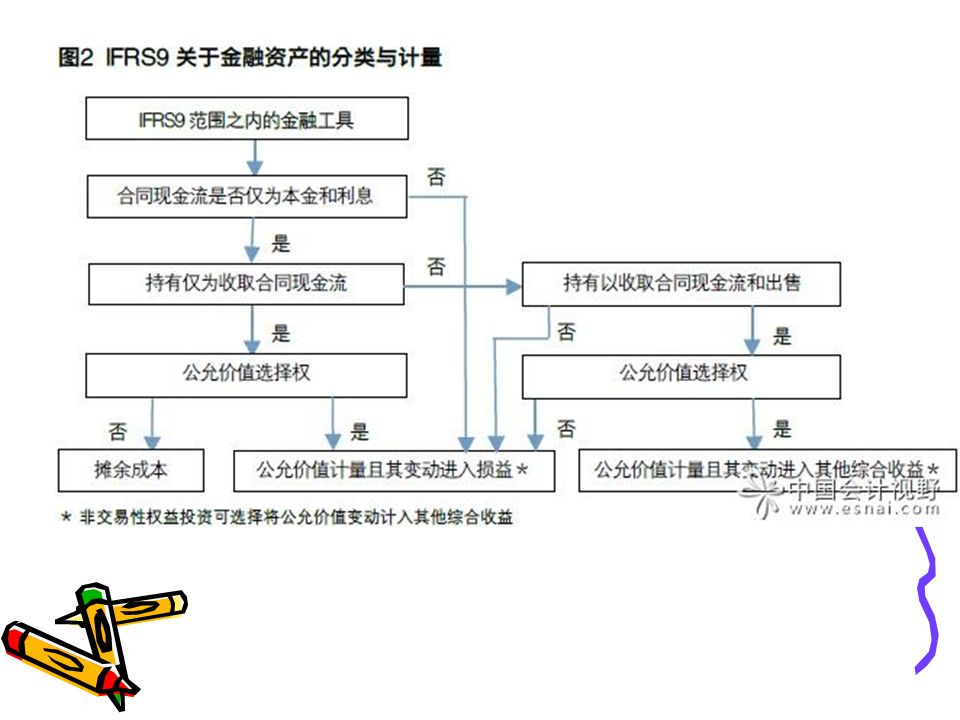

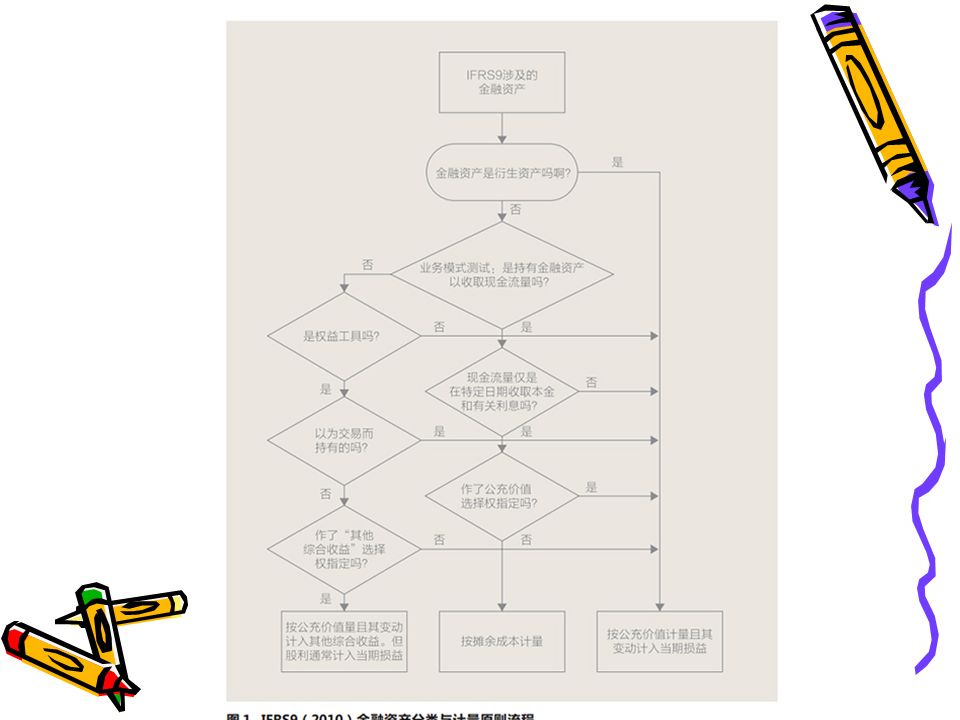

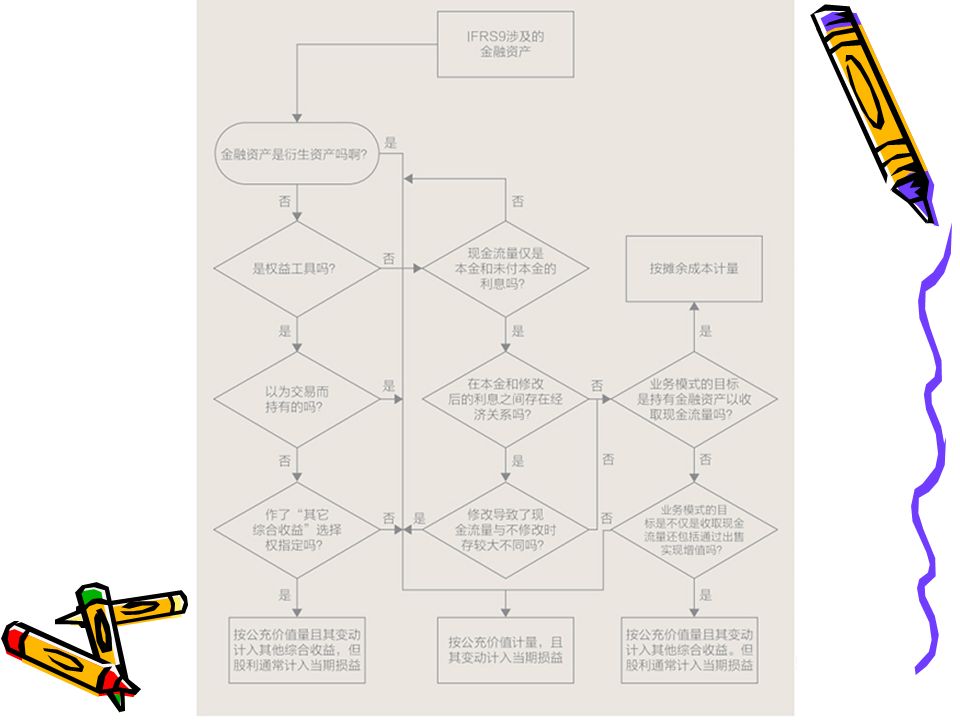

Classification and measurement Business model and contractual characteristics are critical. Initial measurement Amortised cost Fair value

9

Classification and measurement FA – three categories Amortised cost: Business model+ Contractual characteristics FV: (1) Option to report changes to OCI----Equity investments not held for trading (2) FV through P/L

Option to report changes to OCI----Equity investments not held for trading (2) FV through P/L")

10

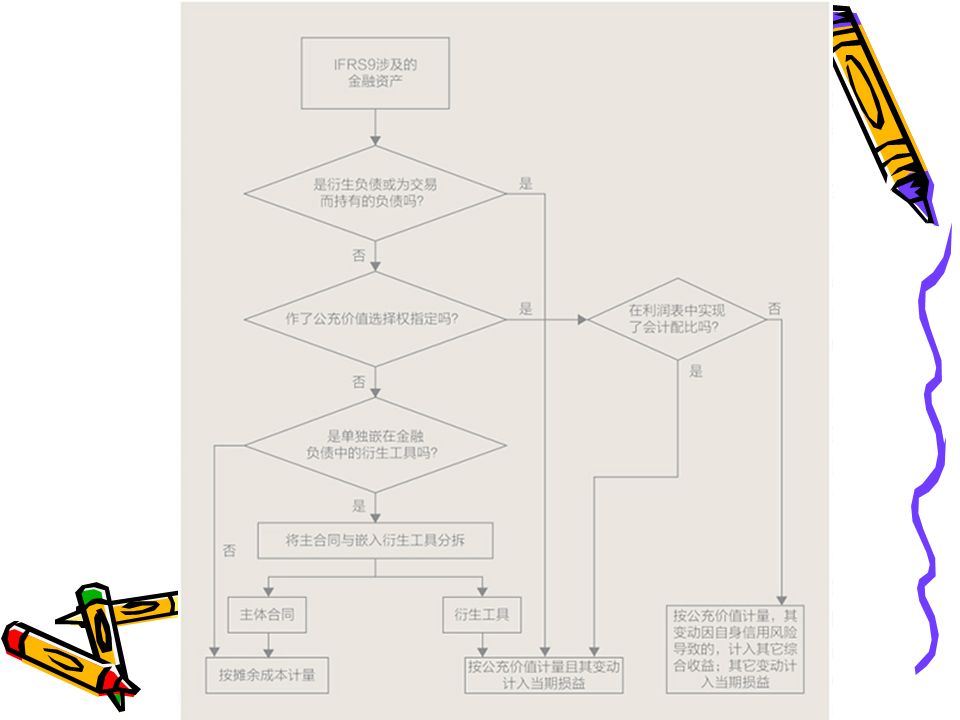

Classification and measurement FL — Three categories Amortised cost (most financial liabilities) FV through P/L Cost

FV through P/L Cost")

12

Impairment Test for impairment at each year end for all FA except for FV through P/L Impairment loss => IS

13

Impairment 例如 : 提供住房抵押贷款,在某国发起一住房贷款组合,图 3 反映了不同阶段预期信用损失的确认情况。

14

Derivatives 1 characteristics (a) its value changes in response to the change in a specified interest rate, financial instrument price, commodity price, foreign exchange rate (b) little cost or no cost and (c) settled at a future date.

its value changes in response to the change in a specified interest rate, financial instrument price, commodity price, foreign exchange rate (b) little cost or no cost and (c) settled at a future date.")

15

衍生金融工具 定义 衍生金融工具是派生的、其价值依赖于基本金融工具的金融工具。 种类 – 远期: – 远期: 是指双方约定在未来的某一确定时间,按确定的价格买卖一定数量 的某种金融资产的合约。 – 期货: – 期货: 是指标准化的远期合约。 – 期权: – 期权: 是指赋予购买者在未来的某一确定时间,按确定的价格买卖一定数 量的某种金融资产权利的合约。 – 互换: – 互换: 是指两个或两个以上当事人按照商定的条件,在约定的时间内,交 换一系列现金流的合约。

16

Derivatives 2 categories: forward contracts (including forward, future and swap) and option contracts. Forward contract gives the entity obligation to buy or sell something in future whereas option only grants the entity rights but no obligation to buy or sell in future.

17

Derivatives 3 purposes Speculation Hedge

18

Hedge Definition Hedge accounting is a risk management technique designed to offset changes in fair value or cash flow

19

Hedge It ’ s optional to apply hedge accounting The main impact of hedge accounting is that gains and losses on the hedging instrument and the hedged item are recognised in the same period.

20

Hedge Conditions to be met: Formal designation and documentation in place The hedge is expected to be highly effective The effectiveness of the hedge can be reliably measured. The hedge is assessed on an ongoing basis and determined to have been highly effective throughout the financial reporting periods for which the hedge was designated. Effectiveness 80% - 125% G/L on Hedging instrument G/L on hedged item

21

Hedge Types of hedge: FV hedge Cash flow hedge

22

Hedge FV hedge changes in FV of the hedged item That is attributable to a particular risk and will affect reported income G/L of hedging instrument and hedged item are recognised in IS as incurred even if the hedged item is measured at other way

23

Hedge Cash flow hedge a hedge of the exposure to variability in cash flow

24

Hedge Accounting treatment The gain or loss on the hedging instrument from “ effective ” hedge should be recognised directly in OCI. If a hedge of a forecast transaction subsequently results in the recognition of a FA or a FL, G/L in OCI shall be reclassified from equity to IS.

25

Hedge If a hedge of a forecast transaction subsequently results in the recognition of a non-financial asset or a non-financial liability entity can either keep deferred gain/loss in reserve and release from reserve as asset or liability realised or deduct the initial CV of asset or liability (basis adjustment).

.")

26

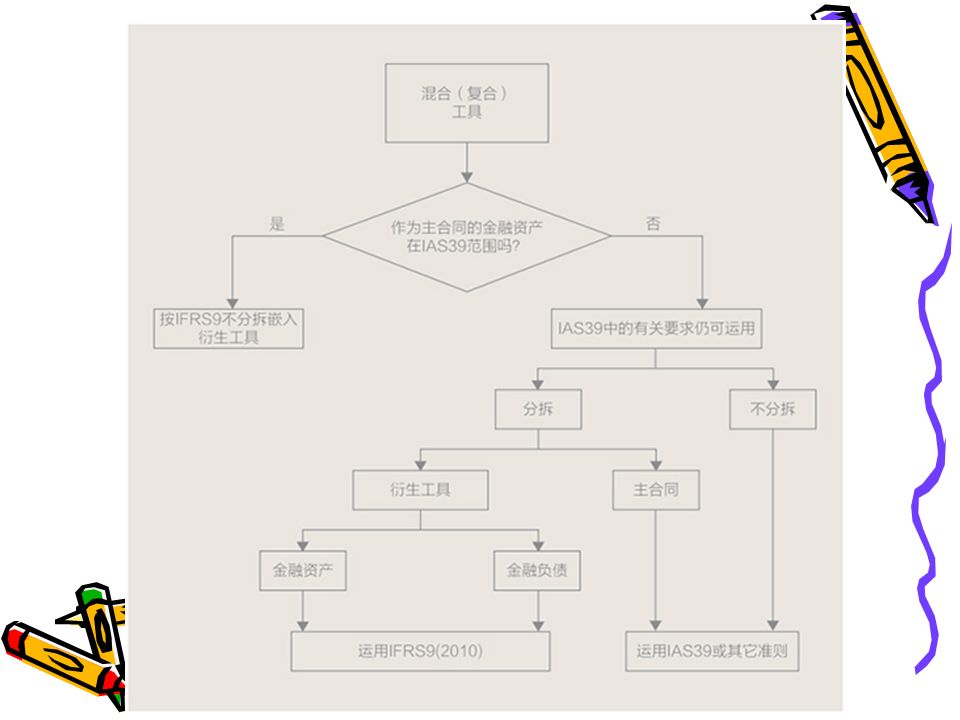

Slide 26 Embedded derivatives Example: Bond redeemable in 5 years' time Part of redemption price based on increase in FTSE 100 index 'Host' contract Bond Embedded derivative Option on equities Accounted for as normal Treated as derivative

27

Embedded derivatives Separation conditions: meets the definition of a derivative. The combined contract is not measured at fair value with changes in fair value recognised in profit or loss.

28

Embedded derivatives Separation conditions: The economic characteristics and risks of the embedded feature are not closely related to those of the host contract.

29

Embedded derivatives The artifacts produced by the company require special packaging materials in order to store and deliver the product. Artright has entered into a one year contract with a local supplier to deliver these materials on a quarterly basis until the end of the contract on 30 November 2005.

30

Embedded derivatives The agreed price of each delivery is £ 100,000 sterling (UK pounds) payable quarterly. Required: Discuss the nature of the contracts to purchase packaging materials.

31

IFRS9 和 IAS39 在套期上的不同 IFRS9 的主要变化涉及被套期项目和套期保值工具的 资格、套期有效性的测试,以及披露要求的扩展。 在被套期项目的资格方面, IFRS9 指出非金融资产和 非金融负债的风险组合只要满足 “ 可单独识别 ” 和 “ 可靠 计量 ” 两个条件,也可被指定为被套期项目( IAS39 只 针对金融项目)。 IFRS9 的这一变化对意欲进行套保的非金融企业报告 主体(如航空公司等非金融企业)非常有利。

。 IFRS9 的这一变化对意欲进行套保的非金融企业报告 主体(如航空公司等非金融企业)非常有利。")

32

IFRS9 和 IAS39 在套期上的不同 在套期工具的资格方面, IFRS9 允许按 公允价值计量且其变动进入损益的非衍 生金融资产或负债作为套期工具 ( IAS39 只允许在外汇风险套期保值中 使用非衍生金融资产或负债)。

。")

33

IFRS9 和 IAS39 在套期上的不同 在套期有效性测试方面,取消了 “ 80%-125% ” 这一衡量套期有效性的量化界限标准,代之通 过复核风险管理策略来评估套期有效性。 IFRS9 并未规定评价套期有效性的具体方法, 既可采用定量评估,也可采用定性评估,报告 主体的风险管理系统是实施评价的主要信息来 源。

38

Thank you !

Similar presentations

>")