Download presentation

Presentation is loading. Please wait.

1

International Settlements 国际结算

2

《国际结算》课程的性质 《国际结算》是国际金融学的一个分支,从微观角度探讨国际间货币运动的理论与实务问题,主要研究结算工具,结算方式和以银行为中心的资金划拨清算,其主要目的在于以最科学,最有效的方法来清算国与国之间以货币表现的债权债务关系.

3

《国际结算》课程的性质 《国际结算》商业银行国际结算业务紧密相关的,注重理论在实际业务中应用,具有很强的专业性和实务可操作性,也是一门适应我国银行业务与国际银行业务接轨需要, 与国际惯例紧密联系,具有很强国际性的专业课程.

4

《国际结算》课程的目的 通过《国际结算》的教学,要求学生能够掌握国际结算的基本理论,基本知识和基本技能;做到理论与实际相结合,能够运用理论知识为指导进行国际结算的实务操作的实用型、实践型、实干型人才。

5

《国际结算》课程所处的位置 先修课程为《货币银行学》、《货币金融学》、《国际金融学》;后续课程包括《外汇银行会计》,《国际融资实务》、《进出口单证实务》等

6

《国际结算》的教学重点 以课堂讲授为主 课程的重点有两个: 一是国际结算方式,即汇款,托收,信用证;

二是国际结算单据.通过案例教学,实训室软件模拟操作,习题练习等办法解决.

7

MOTO与中国移动签订价值4.31亿GSM扩容合同

2008年08月07日 来源:人民网

8

国际社会向四川汶川地震灾区抗震救灾提供援助

2008年,一些国家宣布向四川汶川地震灾区抗震救灾提供援助。 沙特国王阿卜杜拉决定沙特向中方捐赠5000万美元现金和1000万美元物资,帮助中国抗震救灾。 波兰外交部已通过中国红十字会向灾区提供10万美元援助。 2008年05月15日 来源:百度财经

9

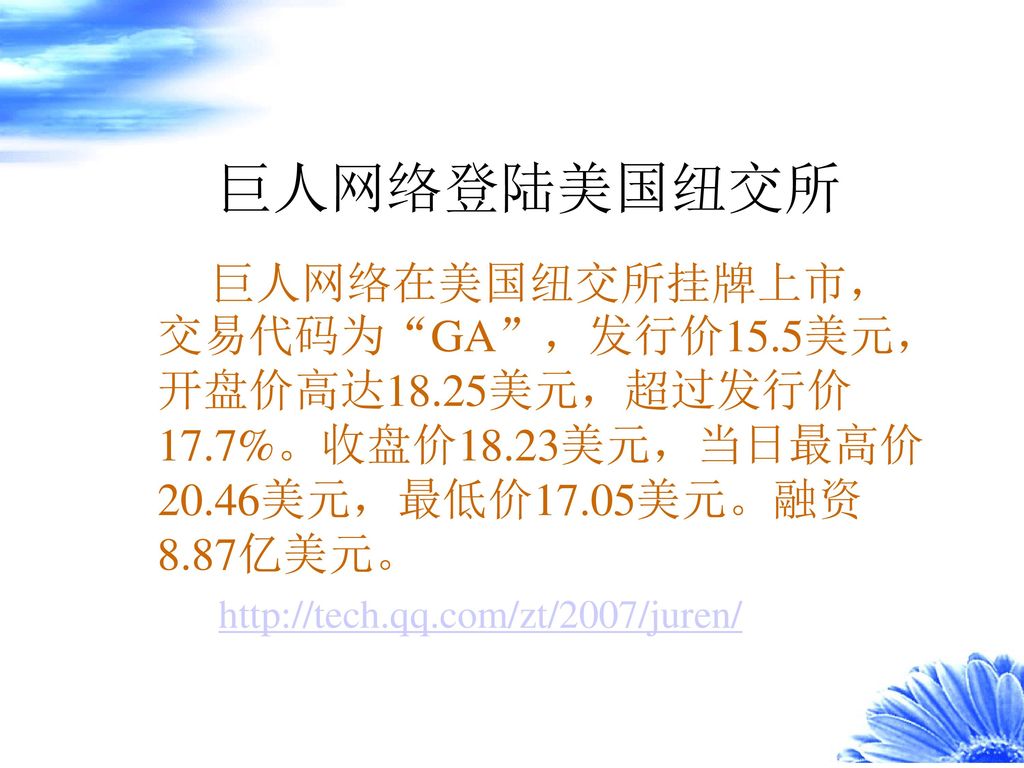

巨人网络登陆美国纽交所 巨人网络在美国纽交所挂牌上市,交易代码为“GA”,发行价15.5美元,开盘价高达18.25美元,超过发行价17.7%。收盘价18.23美元,当日最高价20.46美元,最低价17.05美元。融资8.87亿美元。

10

About the course International settlements is a course of integrated theory(一体化理论) with practice. It puts emphasis on the application of theory into actual business operations.

with practice. It puts emphasis on the application of theory into actual business operations.")

12

Basic procedure of international settlements

Funds Goods/commodities Shipping Co. Goods Exporter/ Seller Importer/ Buyer documents instruments Funds Exporter’s bank Importer’s bank

13

About the course International settlements is also a course of our country' s banking business linking up with the world ' s banking business , it lays stress on handling international business in English in accordance with international practice .

14

Our Purpose For the sake of helping students to learn international settlements and to have a good grasp of basic theory , elementary knowledge and fundamental technical ability of this course ,so we teach partly in English .

15

What will you learn in this course?

1. Three financial instruments: bill of exchange(汇票), promissory note(本票), check (cheque支票) 2. Three main international settlement methods remittance(汇款), collection(托收), letter of credit(信用证) 3. Other documents commercial invoice(发票), transport documents(运输单据), insurance documents(保险单) 4. International customs and practice for international settlements URC522(托收统一规则), UCP600(跟单信用证惯例)

, promissory note(本票), check (cheque支票) 2. Three main international settlement methods. remittance(汇款), collection(托收), letter of credit(信用证) 3. Other documents. commercial invoice(发票), transport documents(运输单据), insurance documents(保险单) 4. International customs and practice for international settlements. URC522(托收统一规则), UCP600(跟单信用证惯例)")

16

How to study this course?

提前预习与课后复习结合; 理论知识与实务操作结合; 考勤和平时作业考察与考试相结合.

17

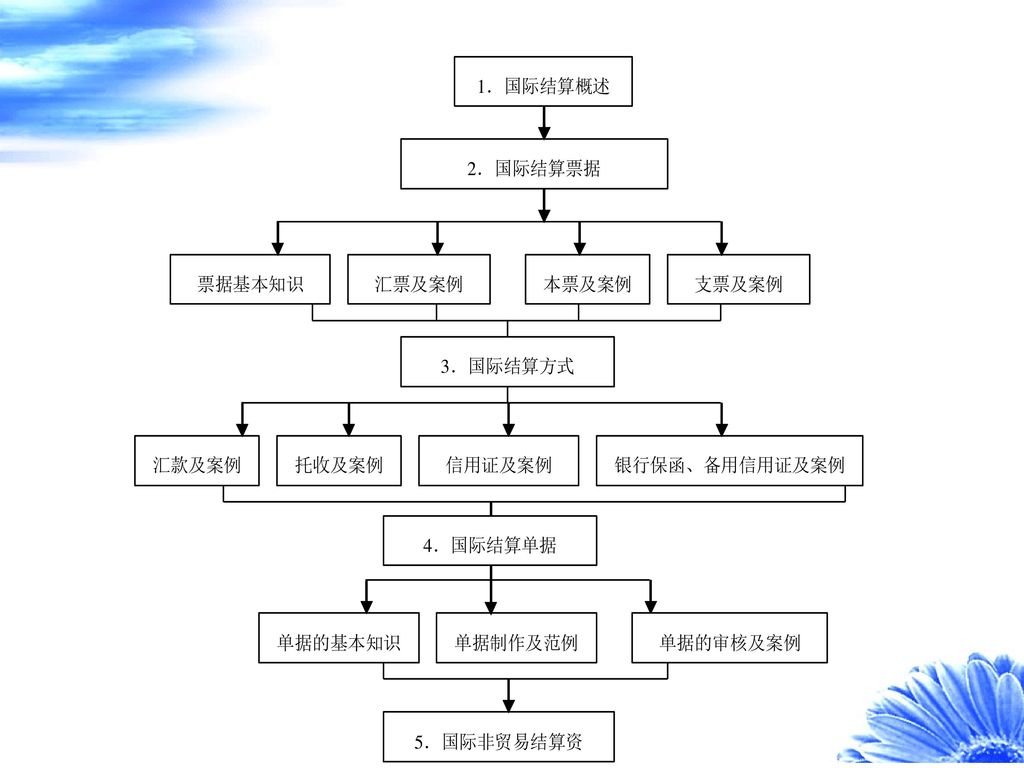

Outline Chapter 1. Introduction to International Settlement

Chapter 2. Instruments Chapter 3. Remittance Chapter 4. Collection Chapter 5. Letters of Credit Chapter 6. Documents Related to International Settlement and Examination Chapter 7. Other Methods of Settlement System Chapter 8. International Non-Trade Finances

19

Chapter 1. Introduction to International Settlement

国际结算概述 Chapter1. Introduction

20

In this chapter,you will learn:

1.1 Definition 1.2 Types of International Settlement 1.3 History and Development of International Settlement 1.4 Major Points Concerning International settlements 1.5 Bank relationships in international Settlements Chapter1. Introduction

21

The origin Most international settlements originate from transaction in the world trade. International political, economic and cultural exchange inevitably leads to credits and debts owed by one country to another. 是一个国家由于对外贸易和经济合作以及政治稳获交流活动而发生的以货币表现的款项收付或债权债务结算。 Chapter1. Introduction

22

Basic procedure of international settlements

Funds Goods/commodities Shipping Co. Goods Exporter/ Seller Importer/ Buyer documents instruments Funds Exporter’s bank Importer’s bank Chapter1. Introduction

23

1.1 Definition International payments and settlements are financial activities conducted among different countries in which payments are effected or funds are transferred from one country to another in order to settle accounts,debts,claims,etc. financial intermediary convertible currency 所谓国际结算,是指为清偿国际间的债权债务关系而发生在不同国家之间的货币收付活动 Chapter1. Introduction

24

Principle for International settlements

Each currency is cleared within the boundary of the issuing country. A Co.(exporter) USA B Co.(importer) Japan Chemical Bank USA Sumitomo Bank Japan Chapter1. Introduction

USA. B Co.(importer) Japan. Chemical Bank. USA. Sumitomo Bank. Japan. Chapter1. Introduction.")

25

Currency: Convertible Currency

(1) Convertible currency in export country. (2) Convertible currency in import country. (3) Convertible currency in third country, generally referred to US currency. Chapter1. Introduction

Convertible currency in export country. (2) Convertible currency in import country. (3) Convertible currency in third country, generally referred to US currency. Chapter1. Introduction.")

26

? ? ? Unconvertible Absolutely currency convertible Limited currency

Chapter1. Introduction

27

Convertible Currency 可兑换货币也称自由外汇,是指一种货币只要不受限制可以自由兑换成其他货币,即为可兑换货币。作为可兑换货币必须具备以下三个条件: (1)它能自由兑换成其他货币; (2)它对国际性经常项目(即贸易与非贸易项目)的支付不受限制; (3)该货币国的管理当局不采用或不实行多种汇率制度或差别汇率制度。 Chapter1. Introduction

它对国际性经常项目(即贸易与非贸易项目)的支付不受限制; (3)该货币国的管理当局不采用或不实行多种汇率制度或差别汇率制度。 Chapter1. Introduction.")

28

国际结算中货币的使用原则: 出口——“硬币”, 进口——“软币” 非贸易收款——“硬币”, 非贸易付款——软币; 引进外资——软币

也就是 收入——“硬币” 支出——“软币” Chapter1. Introduction

29

国 际 结 算 预先付款 方 交单前预付 式 付 款 时 间 装运时付款 交单时付款 装运后付款 交单后付款

Chapter1. Introduction

30

1.2 Types of International Settlement

Most international payments originate from transactions in the world Trade. They are money transfers as a result of international clearing, such as: ⑴ International trade settlement国际贸易结算 ⑵ International non-trade settlement国际非贸易结算 Chapter1. Introduction

31

Ⅱ.Capital and Financial Account Ⅲ.International Reserve

Ⅰ.Current Account 1. Goods & Service a. Goods b. Serviced 2. Income 3. Current Transfer/Unilateral Current Transfer Ⅱ.Capital and Financial Account 1. Capital Account 2.Financial Account (1) Direct Investment (2) Indirect Investment (3) Portfolio Investment (4) Other Investment Ⅲ.International Reserve Ⅳ .Net Error & Omission 经常账户:160,818,311;货物与服务:124, ;货物:134, ;服务:-9,391,392; 资本与金融账户:62.963,916;资本:4,101,792;金融账户:58,862,124 储备资产:-207,016(2005年中国国际收支数据,单位:千美元)

Direct Investment. (2) Indirect Investment. (3) Portfolio Investment. (4) Other Investment. Ⅲ.International Reserve. Ⅳ .Net Error & Omission. 经常账户:160,818,311;货物与服务:124, ;货物:134, ;服务:-9,391,392; 资本与金融账户:62.963,916;资本:4,101,792;金融账户:58,862,124. 储备资产:-207,016(2005年中国国际收支数据,单位:千美元)")

32

(1) International trade settlement国际贸易结算

With the expansion of global trade amongst countries, the role of banks, in international trade finance is becoming more and more important. Most transactions must be settled through banks. Without the bank’s participation,international trade would not have been developed to the stage we have reached today. Chapter1. Introduction

33

International Trade 1.Major participants : 2.Sale contract:

buyer seller banks 2.Sale contract: quality clause quantity clause package clause price clause delivery terms insurance clause payment clause Commodity inspection clause 3. Trade terms:Incoterms 2010, 13 terms Chapter1. Introduction

34

Sale contract Seller: address, telex/fax; Buyer:address, telex/fax

Goods Quality clause:the goods description, quality,specifications Quantity clause:weight, numbers, length, dimension, volume, capacity Packing clause:mode of packing, and its material Price clause:unit price, pricing currency , price terms used Deliver terms:time of delivery, port of loading and destination, transshipment, partial shipment ,mode of transportation Insurance clause:risks to be covered, the percentage of insurance Payment clause:payment method and its content Commodity inspection clause:how the right of inspection is determined,k the time, place and organization of inspection Claim clause , arbitration clause & force majeure clauses

35

EXW EX WORKS(…named place)工厂交货条件 FCA FREE CARRIER(… named place)交至承运人条件 FAS FREE ALONGSIDE SHIP (… named port of shipment)船边交货条件 FOB FREE ON BOARD (… named port of shipment)装运港船上交货条件 CFR COST AND FREIGHT (… named port of destination)成本加运费条件 CIF COST, INSURANCE AND FREIGHT (… named port of shipment)成本加运保费交货条件 CPT CARRIAGE PAID TO (… named port of shipment)运费付至——交货 CIP CARRIAGE AND INSURANCE PAID TO (… named port of shipment) 运保费付至——交货条件 DAT Delivered At Terminal (… named place)目的港交货条件 DAP (new delivery term) Delivered At Place 特定地点交货条件 DDP DELIVERED DUTY PAID (… named port of shipment)完税交货条件

装运港船上交货条件. CFR. COST AND FREIGHT (… named port of destination)成本加运费条件. CIF. COST, INSURANCE AND FREIGHT (… named port of shipment)成本加运保费交货条件. CPT. CARRIAGE PAID TO (… named port of shipment)运费付至——交货. CIP. CARRIAGE AND INSURANCE PAID TO (… named port of shipment) 运保费付至——交货条件. DAT. Delivered At Terminal (… named place)目的港交货条件. DAP. (new delivery term) Delivered At Place 特定地点交货条件. DDP. DELIVERED DUTY PAID (… named port of shipment)完税交货条件.")

36

(2) International non-trade settlement国际非贸易结算

There are many ways by which funds can be transferred from one country to another under trade service. When the tourists, merchants, delegations or other people go abroad, they need money to spend, to buy something, or to pay for various expenses and charges there. The most common means for them to carry funds are cash , traveler’s check, traveler’s letter of credit and credit card. These are within the scope of non-trade settlement. Chapter1. Introduction

37

How many international transactions can you list?

visible trade有形贸易 invisible trade无形贸易 financial transaction金融交易 overseas remittances 海外汇款 educational expenses教育开支 inheritances遗产继承 Chapter1. Introduction

38

How many international transactions can you list?

technology transfer技术转让 patent 专利 copyright contract版权合同 foreign exchange market transactions金融市场交易 export credits出口信贷 syndicated loans辛迪加贷款 international bond 国际债券 Chapter1. Introduction

39

1.3 History and Development of International Settlement

(1) From cash settlement to non-cash settlement从现金结算到非现金结算 (2) From direct payment made between international traders to payment effected through a financial intermediary从贸易商之间直接支付到通过金融中介进行支付 (3) From payments under simple price terms to payments under more complex price terms从使用简单贸易术语结算到复杂贸易术语的结算 (4) Internet era互联网的结算 Chapter1. Introduction

From cash settlement to non-cash settlement从现金结算到非现金结算. (2) From direct payment made between international traders to payment effected through a financial intermediary从贸易商之间直接支付到通过金融中介进行支付. (3) From payments under simple price terms to payments under more complex price terms从使用简单贸易术语结算到复杂贸易术语的结算. (4) Internet era互联网的结算. Chapter1. Introduction.")

40

(1)From cash settlement to non-cash settlement

Instruments Bill of exchange Promissory Note Cheque/check Non-Cash Settlement非现金结算 13 century A.D. Exchange for GBP1, Beijing,1 April,2003 At sight pay to the order of DEF Co.the sum of Pounds one thousand two hundred and fifty only To XYZ Bank, For ABC Co., Beijing London (signature) Expensive Risky Turnover of funds slow End of 18 century Foreign exchange bank

Expensive. Risky. Turnover of funds slow. End of 18 century. Foreign exchange bank.")

41

Non-cash settlement非现金结算

From the thirteenth century A.D., bills of exchange were created, gradually taking the place of coins in international payments, and the bill of exchange market began to develop. Chapter1. Introduction

42

13 century A.D. end of 18 century A.D. Bill of exchange

Foreign exchange bank Foreign exchange market Chapter1. Introduction

43

(2)From direct payment made between international traders to payment effected through a financial intermediary With the worldwide banking network and modern banking technicality, banks can not only provide easy and quick transfer of funds needed for conducting international trade but also furnish their customers with valuable economic and credit information. Chapter1. Introduction

44

(3)From simple price terms to more complex price terms

In the past, international trade payments were settled on very simple price terms, such as cash on delivery, cash on shipment, cash with order, cash before shipment, etc. In modern international trade, a more comprehensive and exact set of terms has been developed. As indicated in INCORTERMS2010(International Rules for the Interpretation of Trade Terms)ICC Publication, the price terms available for use are multifarious and more complicated than before. 多种的,各式各样的 Chapter1. Introduction

ICC Publication, the price terms available for use are multifarious and more complicated than before. 多种的,各式各样的. Chapter1. Introduction.")

45

(4)Internet era With the development of computer technology, business is done and payments and settlements are effected by means of all kinds of payment systems, which makes it quicker and safer and more convenient for both the Buyer and Seller. Nowadays, Internet is developing very fast. This new type of business transaction is called net banking. Although there are a lot of problems to be solved,net banking is very promising. Chapter1. Introduction

46

communication meshwork/network

环球银行间金融电讯协会 纽约清算所交换银行相互收付系统 SWIFT CHIPS CHAPS FEDWIRE 伦敦交换银行 自动收付系统 联邦储备 清算系统 Chapter1. Introduction

47

SWIFT:The Society For Worldwide Inter-bank Financial Telecommunications(环球银行间金融电讯协会)

中国是SWIFT会员国。中国银行作为中国的外汇外贸专业银行于1983年2月加入SWIFT,成为中国第一家会员银行,1985年5月13日,中国银行正式开通SWIFT。

48

20世纪90年代开始,中国所有可以办理国际金融业务的国有商业银行、外资和侨资银行以及地方银行纷纷加入SWIFT。

1996年中国SWIFT发报增长率为42.2%,在SWIFT全球增长率排名第一,中国银行在SWIFT前40家大用户中排名34位。 中国银行每日SWIFT发报量达3万多笔,采用SWIFT方式进行收发电报已占到全行电讯总收付量的90%。 SWIFT网络是国际结算、收付清算、外汇资金买卖、国际汇兑等各种业务系统的通讯主渠道,部分业务实现了自动化处理。 chaining(SWIFT study):

:")

49

Characteristics 1.SWIFT needs member qualification.

2.SWIFT’s charge is low. It’s about 18% of that used by telex, and 2.5% of that used by cable. 3.SWIFT is safer. (SWIFT authenticate key) 4.SWIFT has standard uniform format. Chapter1. Introduction

4.SWIFT has standard uniform format. Chapter1. Introduction.")

50

加入SWIFT的中国境内银行 Bank Identified code Bank of China BKCH CN BJ

The Industrial and Commercial ICBK CN BJ The Agricultural Bank of China ABOC CN BJ The Investment Bank of China IBOC ON BJ The Communication Bank of China COMM CN BJ China Construction Bank PCBC CN BJ The People’s Bank of China PBOC CN BJ China Citic Bank CIBK CN BJ America Bank , Shanghai Branch BOFX CN SX HongKong and Shanghai Banking Corporation, Ltd. HSBC CN SX

51

CHIPS:Clearing House Interbank Payments System.(跨国美元支付系统)

1970年4月成立,国际美元支付系统。它是一个著名的私营跨国大额美元支付系统,是跨国美元交易的主要结算渠道。 通过CHIPS处理的美元交易额约占全球美元总交易额的95%。 CHIPS成员有纽约清算所协会会员、纽约市商业银行、外国银行在纽约的分支机构等。 CHIPS是一个净额支付清算系统,它租用了高速传输线路,有一个主处理中心和一个备份处理中心。每日营业终止后,进行收付差额清算,每日下午六时(纽约时间)完成资金转账。

完成资金转账。")

52

CHAPS: Clearing House Automated Payment System

Chapter1. Introduction

53

FEDWIRE: Federal Reserves Wire Transfer System(全美境内美元支付系统)

由于该系统有专用的实现资金转移的电码通讯网络,权威性、安全性较高。此外它还承担着美联储货币政策操作及政府债券买卖的重要任务。 它每日运行18个小时,每笔大额的资金转账从发起、处理到完成,运行全部自动化。

54

1.4 Major Points Concerning International settlements

(1) International settlements methods (2) The financial instrument that facilitate International settlements (3) Documents used in International settlements (4) The currencies used in international settlements. (5) Rules and regulations on international make sure they are different URC522:Uniform Rules for Collection Chapter1. Introduction UCP500:Uniform Customs and Practice for documentary credit

International settlements methods. (2) The financial instrument that facilitate. International settlements. (3) Documents used in International settlements. (4) The currencies used in international. settlements. (5) Rules and regulations on international. make sure they are different. URC522:Uniform Rules for Collection. Chapter1. Introduction. UCP500:Uniform Customs and Practice for documentary credit.")

55

国际结算的基本要素 1、银行合作是办理国际结算业务的关键所在。(结算路径)

2、现代化的支付和通讯系统保证了资金顺畅、快速地跨国流动。(结算路径) 3、票据是国际结算中主要支付工具。(结算工具) 4、单据是实现物权转移与债务清偿的重要依据。(结算工具) 5、国际结算方式是最终实现货币跨国收付的手段。(结算方式) Chapter1. Introduction

3、票据是国际结算中主要支付工具。(结算工具) 4、单据是实现物权转移与债务清偿的重要依据。(结算工具) 5、国际结算方式是最终实现货币跨国收付的手段。(结算方式) Chapter1. Introduction.")

56

1.5 Bank relationships in international Settlements

(1)Sister’s Bank/overseas branch海外分行 (2)Representative Bank (Correspondent)代理行 (3)Accounting Bank账户行 Chapter1. Introduction

Sister’s Bank/overseas branch海外分行. (2)Representative Bank (Correspondent)代理行. (3)Accounting Bank账户行. Chapter1. Introduction.")

57

The Worldwide Network of Banks

1、 Representative Office(代表处) 2、 Agency Office(代理处) 3、 Overseas Sister Bank/Branch, Sub branch(海外分、支行(境外联行)) 4、 Correspondent Banks(代理银行) 5、 Subsidiary Banks(附属银行(子银行)) 6、 Affiliated Banks(联营银行) 7、 Consortium Bank(银团银行) Chapter1. Introduction

2、 Agency Office(代理处) 3、 Overseas Sister Bank/Branch, Sub branch(海外分、支行(境外联行)) 4、 Correspondent Banks(代理银行) 5、 Subsidiary Banks(附属银行(子银行)) 6、 Affiliated Banks(联营银行) 7、 Consortium Bank(银团银行) Chapter1. Introduction.")

58

Bank of China Overseas branch

59

(2)Representative Bank (Correspondent)代理行

International banking is effected through the cooperation of commercial banks all over the world. This cooperation comes from the establishment of correspondent relationships between banks. The so-called correspondent bank may be defined as “a bank having direct connection or friendly service relations with another bank”. Chapter1. Introduction

60

The bank may open deposit accounts with, and entrust business to each other on a reciprocal basis.

互惠的,相应的 信赖,信托,交托 Chapter1. Introduction

61

When selecting a bank as a correspondent bank, what factors should be taken into account?

⑴The reputation of the bank; ⑵ Size of the bank; ⑶ Location of the bank; ⑷ Services offered by the bank; ⑸ Fundamental policies and strength of the bank; ⑹ Physical features and personnel; ⑺ Momentum of early start, etc. Chapter1. Introduction

62

Agency arrangement Control documents

Establish a correspondent relationship between two banks. Agency arrangement Control documents What do control documents include? Chapter1. Introduction

63

Control Documents Lists of specimen of authorized signatures印鉴

Verify the messages, letters(airmailed) are authentic Telegraphic test keys密押 Verify the telex and cable are authentic Terms and conditions费率表 SWIFT authentic key验证码 是银行列示的所有有权签字的人的有权签字额度、签字范围、有效签字组合方式以及亲笔签字字样。代理行可凭其核对对方银行发来的电报、电传等的真实性。 是两家代理行之间事先约定的专用押码,在发送电报时,由发送电报的银行在电文前面加注,经接受电报的银行核对相符,用以确认电报的真实性。 Chapter1. Introduction

are authentic. Telegraphic test keys密押. Verify the telex and cable are authentic. Terms and conditions费率表. SWIFT authentic key验证码. 是银行列示的所有有权签字的人的有权签字额度、签字范围、有效签字组合方式以及亲笔签字字样。代理行可凭其核对对方银行发来的电报、电传等的真实性。 是两家代理行之间事先约定的专用押码,在发送电报时,由发送电报的银行在电文前面加注,经接受电报的银行核对相符,用以确认电报的真实性。 Chapter1. Introduction.")

64

Bank of China 服务项目 收费标准 现钞托收 进口托收 跟单托收 汇出境外汇款

电汇 汇款金额的 1‰,最低50元/笔,最高1000元/笔,另加收电讯费 票汇、信汇 汇款金额的 1‰,最低100元/笔,最高1200元/笔,另加收邮费(如有) 外币光票托收 光票托收 托收金额的 1‰,最低50元/笔,最高1000元/笔,另加收邮费 买入外币票据 买入票据 票据金额的 7.5‰,最低50元/笔 现钞托收 100元/笔,另加收邮费 进口托收 进口代收金额的 1‰,最低100元/笔,最高2000元/笔 跟单托收 代收金额的 1‰,最低100元/笔,最高2000元/笔,另加收邮费

外币光票托收. 光票托收. 托收金额的 1‰,最低50元/笔,最高1000元/笔,另加收邮费. 买入外币票据. 买入票据. 票据金额的 7.5‰,最低50元/笔. 现钞托收. 100元/笔,另加收邮费. 进口托收. 进口代收金额的 1‰,最低100元/笔,最高2000元/笔. 跟单托收. 代收金额的 1‰,最低100元/笔,最高2000元/笔,另加收邮费.")

65

(3)Inter-bank account A current account or a checking account may be opened between banks with the establishment of a correspondent banking relationship. Any bank before opening an account in its correspondent bank, must be aware of the detailed conditions of this connection, such as amount of initial deposit, minimum credit balance for covering the cost of services provided, interest rate of the account, overdraft permission, and how often the statement of account is sent. Chapter1. Introduction

66

账户行 存款客户 Current a/c XXX Current a/c XXX 开户行 账户行 Depository Depositor

Bank Depositor Current a/c XXX Depositor Bank Depository Bank 开户行 账户行 Chapter1. Introduction

67

①Nostro account往账 The Italian word “Nostro” means “our”. Nostro account is the foreign currency account(due from account)of a major bank with the foreign banks abroad to facilitate international payments and settlements.我行在它行开立的存款账户 ②Vostro account来账 The Italian word “Vostro” means “your”. The Italian word “Vostro” means “your”. Vostro account is an account(due to account)held by a bank on behalf of a correspondent bank.它行在我行开立的存款账户 Chapter1. Introduction

of a major bank with the foreign banks abroad to facilitate international payments and settlements.我行在它行开立的存款账户. ②Vostro account来账. The Italian word Vostro means your . The Italian word Vostro means your . Vostro account is an account(due to account)held by a bank on behalf of a correspondent bank.它行在我行开立的存款账户. Chapter1. Introduction.")

68

往账 Nostro account: is the foreign currency account (due from account) of a major bank with the foreign banks abroad to facilitate international settlements. From the point of Bank of China, a nostro account is our bank’s account in the books of an overseas bank, denominated in foreign currency. Bank of New York Bank of China USD Account Chapter1. Introduction

of a major bank with the foreign banks abroad to facilitate international settlements. From the point of Bank of China, a nostro account is our bank’s account in the books of an overseas bank, denominated in foreign currency. Bank of New York. Bank of China. USD. Account. Chapter1. Introduction.")

69

A/C XXX is A Bank’s __________________a/c

Current a/c XXX A Bank B Bank B Bank’s currency Nostro A/C XXX is A Bank’s __________________a/c Chapter1. Introduction

70

Banking Corporation,Ltd.,

来账 Vostro account: is the domestic currency account (due to account) held by a bank on behalf of a correspondent bank. From the point of view of Bank of China, a vostro account is an overseas bank’s account with us, denominated in RMB. Hongkong and Shanghai Banking Corporation,Ltd., Hong Kong Bank of China RMB Account Chapter1. Introduction

held by a bank on behalf of a correspondent bank. From the point of view of Bank of China, a vostro account is an overseas bank’s account with us, denominated in RMB. Hongkong and Shanghai. Banking Corporation,Ltd., Hong Kong. Bank of China. RMB. Account. Chapter1. Introduction.")

71

Exercise: Current a/c XXX A Bank’s currency

B Bank A Bank’s currency A/C XXX is A Bank’s __________________a/c, Vostro Chapter1. Introduction

72

Chapter 2. Instruments 信用工具 Chapter2. Instruments

73

In this chapter,you will learn:

2.1 credit instrument 2.1.1Definition of credit instrument 2.1.2The functions of a negotiable instrument 2.1.3The characteristics of each instrument 2.1.4Instruments law system 2.2 The three important negotiable instruments: Bill of exchange,promissory note and cheque, The essentials of each instrument Chapter2. Instruments

74

2.1 credit instrument 2.1.1 Definition of credit instrument

A credit instrument is a written or printed paper by means of which funds are transferred from one person to another. Credit instruments most commonly used in international payments and settlements are bills of exchange, promissory notes and checks. They are also known, negotiable instruments. Credit instruments may also take such forms as traveler’s cheque, certificates of deposit,treasury bills, treasury bonds, etc. Chapter2. Instruments

75

Instruments characteristic:

1)Negotiability 2)Non-causative Nature 3)Requisite in Form 4)Presentment 5)Return-ability 流通性 无因性 要式性 提示性 返还性 Chapter2. Instruments

Negotiability. 2)Non-causative Nature. 3)Requisite in Form. 4)Presentment. 5)Return-ability. 流通性. 无因性. 要式性. 提示性. 返还性. Chapter2. Instruments.")

76

Negotiable instrument in broad sense

Two words relative to transfer a negotiable instrument A negotiable instrument is a chose in action, the full and legal title to which is transferable by delivery of the instrument (possibly with the transferor’s endorsement) with the result that complete ownership of the instrument and all the property it represents passes freely from equities to the transferee, providing the latter takes the instrument in good faith and for value. Negotiable instrument in broad sense Chapter2. Instruments

with the result that complete ownership of the instrument and all the property it represents passes freely from equities to the transferee, providing the latter takes the instrument in good faith and for value. Negotiable instrument in broad sense. Chapter2. Instruments.")

77

流通票据是一种法定的财产,这种财产的全部或法定的权益可以通过交付进行转让(可以凭转让方的背书),其转让的结果是只要受让人是正当取得或者支付对价而取得该财产,该票据的全部所有权及其所代表的财产权益将转移给受让人。 Chapter2. Instruments

78

conprehensive 广义的票据 泛指一切有价证券和各种凭证 以支付金钱为目的的 可以转让流通的特种证券 狭义的票据 狭义票据是国际结算的重要工具: Bill of Exchange(汇票)、Promissory Note(本票)和Cheque(支票)。 Chapter2. Instruments

79

Instruments characteristic:

1) Negotiability流通性 A negotiable bill may be payable to the order of a specified person. A negotiable bill may be payable to bearer. A bill on which the only or last endorsement is an endorsement in blank may be negotiable. A bill payable to a specified person does not contain words prohibiting transfer or indicating an intention that it should not be transferable , it may also be negotiable. Chapter2. Instruments

Negotiability流通性. A negotiable bill may be payable to the order of a specified person. A negotiable bill may be payable to bearer. A bill on which the only or last endorsement is an endorsement in blank may be negotiable. A bill payable to a specified person does not contain words prohibiting transfer or indicating an intention that it should not be transferable , it may also be negotiable. Chapter2. Instruments.")

80

Kinds of negotiable instrument

in broad sense •Bill of exchange 汇票 • Check/cheque支票 • Promissory Note本票 • Dividend warrant 股利单 • Bearer bond 不记名债券(流通债券) • Bearer scrips 持有人凭证 • Debenture payable to bearer 不记名信用债券 • Share warrant payable to bearer 不记名股份证书 • Treasury bill 国库券 • Certificate of deposit 存单 Chapter2. Instruments

• Bearer scrips 持有人凭证. • Debenture payable to bearer 不记名信用债券. • Share warrant payable to bearer 不记名股份证书. • Treasury bill 国库券. • Certificate of deposit 存单. Chapter2. Instruments.")

81

Instruments characteristic:

2)Non-Causative Nature无因性 The reason(s) of issue or endorse need not to write on the face of the bill. 3) Requisite in Form要式性 The bill must contains the prerequisite items required by the law. Chapter2. Instruments

Non-Causative Nature无因性. The reason(s) of issue or endorse need not to write on the face of the bill. 3) Requisite in Form要式性. The bill must contains the prerequisite items required by the law. Chapter2. Instruments.")

82

Instruments characteristic:

4)presentment提示性 Present for payment Present for acceptance 5)Return ability返还性 Return them back to issuer Chapter2. Instruments

presentment提示性. Present for payment. Present for acceptance. 5)Return ability返还性. Return them back to issuer. Chapter2. Instruments.")

83

Functions of Instruments

1) As a means of payment 2) As a credit instrument 3) As a transferable instrument Chapter2. Instruments

As a means of payment. 2) As a credit instrument. 3) As a transferable instrument. Chapter2. Instruments.")

84

Instruments law system

1)British and USA legal system:the British Commonwealth of Nations and USA. * British Legal System “Bill of Exchange Act”,1882, drafted by Chambers; Article 1~72: Bill of Exchange Article 73 ~82: Cheque Article 83 ~89: Promissory Note Article 90 ~97: Cheque (1957 Revision) * USA legal system “Uniform Negotiable Instrument Law,drafted by Crawford; “Uniform Commercial Code”: Chapter 3:Commercial Paper Chapter2. Instruments

British and USA legal system:the British Commonwealth of Nations and USA. * British Legal System. Bill of Exchange Act ,1882, drafted by Chambers; Article 1~72: Bill of Exchange. Article 73 ~82: Cheque. Article 83 ~89: Promissory Note. Article 90 ~97: Cheque (1957 Revision) * USA legal system. Uniform Negotiable Instrument Law,drafted by Crawford; Uniform Commercial Code : Chapter 3:Commercial Paper. Chapter2. Instruments.")

85

Instruments law system

2)Continental legal system: the main countries in the European Continent. *“Uniform Law for Bills of Exchange and Promissory Notes”, signed at Geneva, 1930 *“Uniform Law for Cheques”, signed at Geneva, 1931 Chapter2. Instruments

Continental legal system: the main countries in the European Continent. * Uniform Law for Bills of Exchange and Promissory Notes , signed at Geneva, * Uniform Law for Cheques , signed at Geneva, Chapter2. Instruments.")

86

2.2 The three important negotiable instruments:

(1) Bill of exchange汇票 (2) Promissory note 本票 (3) Cheque 支票 Chapter2. Instruments

Bill of exchange汇票. (2) Promissory note 本票. (3) Cheque 支票. Chapter2. Instruments.")

87

Review——回顾 一、Definition of credit instrument票据的概念? conprehensive 广义的票据

泛指一切有价证券和各种凭证 以支付金钱为目的的 可以转让流通的特种证券 狭义的票据 狭义票据是国际结算的重要工具: Bill of Exchange(汇票)、Promissory Note(本票)和Cheque(支票)。 Chapter2. Instruments

、Promissory Note(本票)和Cheque(支票)。 Chapter2. Instruments.")

88

2)Non-causative Nature 3)Requisite in Form 4)Presentment

二、票据的特性: 1)Negotiability 2)Non-causative Nature 3)Requisite in Form 4)Presentment 5)Return-ability 流通性 无因性 要式性 提示性 返还性 Chapter2. Instruments

Negotiability. 2)Non-causative Nature. 3)Requisite in Form. 4)Presentment. 5)Return-ability. 流通性. 无因性. 要式性. 提示性. 返还性. Chapter2. Instruments.")

89

Chapter2. Instruments

90

Maker and payer are the same person

Promissory Note For USD99, New York, April 1, 2001 On the 20th June 2001 fixed by the promissory note we promise to pay BA the sum Of ninety-nine thousand nine hundred and ninety-nine US Dollars only For and on behalf of DC (signed) we promise to pay Maker and payer are the same person Chapter2. Instruments

we promise to pay. Maker and payer. are the same person. Chapter2. Instruments.")

91

支票存根 Chapter2. Instruments

92

第二节 汇票 一、Bill of Exchange /Draft/Exchange汇票的定义

第二节 汇票 一、Bill of Exchange /Draft/Exchange汇票的定义 二、Essentials of a bill of exchange汇票的要式项目 三、Acts of a bill of exchange汇票的票据行为 四、Types of bill of exchange汇票种类 Chapter2. Instruments

93

Chapter2. Instruments

94

一、汇票Bill of Exchange /Draft/Exchange

As in the Bills of Exchange Act 1882 A bill of exchange is an unconditional order in writing, addressed by one person to another, signed by the person giving it, requiring the person to whom it is addressed to pay on demand or at a fixed or determinable future time a sum certain in money to or to the order of a specified person , or to the bearer. 汇票是由出票人向另一人签发的,要求即期、定期或在可以确定的将来的时间,向某人或其指定人或来人无条件地支付一定金额的书面命令。 Chapter2. Instruments

95

Three basic parties drawer出票人 drawee Payee 收款人 payer 付款人 issue

Present for acceptance drawee Payee 收款人 Present for payment payer 付款人 Chapter2. Instruments

96

How to understand the definition of a bill of exchange?

⑴Nature: unconditional order in writing ⑵ Basic three parties ⑶ Tenor ⑷ Amount drawer drawee payee on demand/at sight fixed future time determinable future time amount in figures amount in words Chapter2. Instruments

97

二、 Essentials of a bill of exchange汇票的基本项目(必要项目)

①The word “Exchange”汇票字样 ②An unconditional order in writing无条件支付命令 ③ Amount 金额 ④Tenor 付款期限 ⑤ Date and place of Issue出票时间地点 ⑥Name and address of the drawee 付款人名称地址 ⑦Name or business entity of the payee 收款人名称 ⑧Drawer’s signature(s)出票人签名 Chapter2. Instruments

出票人签名. Chapter2. Instruments.")

98

specimen ①汇票字样 ③ 金额 ⑦收款人 Chapter2. Instruments ②无条件支付命令 ⑤ 出票时间地点

③ 金额 ④Tenor 付款期限 ⑦收款人 名称地址 ⑧出票人及签名 ⑥付款人名称地址 Chapter2. Instruments

99

② An unconditional order in writing

*Unconditional:Condition terms cannot be accepted. *Order: It must be expressed in command . *In writing: You can draw and read a bill of draft. Chapter2. Instruments

100

*Order:Correct writing

须用祈使句型: At___________ sight pay to AAA Co. or order the sum of five thousand US dollars only。 而不应使用带有“I should be please if you would kindly pay…”等虚拟文句。 Chapter2. Instruments

101

*Unconditional:Condition terms cannot be accepted.

不允许出现任何限制支付的文句或附带条件。 如“Pay to B Company one thousand US dollars after it makes a blank endorsement on the back of the draft” 即不符合汇票的这一要式规定 Chapter2. Instruments

102

*Unconditional:Condition terms cannot be accepted.

若支付命令指示从某特定账户中支付款项,如“Pay B company the sum of one thousand US dollars from your N0.3 account”, 表明汇票款项的支付取决于该账户中是否有足够的款额,所以该项命令违背了“无条件支付”要式规定。 Chapter2. Instruments

103

*Unconditional:Condition terms cannot be accepted.

汇票中加列表明汇票开立原因的出票条款,如在国际贸易结算中,出票人常在汇票中加列诸如“Drawn under documentary credit N of C Bank”之类出票条款, 仍符合无条件支付命令的要式规定。此类汇票仍具有法律效力。 Chapter2. Instruments

104

Make choice of whether the following bills are

acceptable or not. Mark “X” before acceptable or unacceptable you choose. Explain the reason how do you make the choice? (1) A bill shows : Pay to ABC Co. providing the goods in compliance with contract No. 123 the sum of one thousand US dollars. It is □acceptable/□unacceptable X Chapter2. Instruments

A bill shows : Pay to ABC Co. providing the. goods in compliance with contract No. 123 the. sum of one thousand US dollars. It is □acceptable/□unacceptable. X. Chapter2. Instruments.")

105

It is □acceptable/□unacceptable.

(2) A bill shows: Pay to ABC Co. the sum of ten thousand US dollars on condition that shipment of goods has been made. It is □acceptable/□unacceptable. (3) A bill shows: Pay from our No. 2 account to ABC Co. the sum of one thousand US dollars. X X Chapter2. Instruments

A bill shows: Pay to ABC Co. the sum of ten thousand US dollars on condition that shipment of goods has been made. It is □acceptable/□unacceptable. (3) A bill shows: Pay from our No. 2 account to ABC Co. the sum of one thousand US dollars. X. X. Chapter2. Instruments.")

106

It is □acceptable/□unacceptable.

(4) A bill shows: Pay to ABC Co. the sum of one thousand US dollars and charge\debit same to applicant’s account maintained with you. It is □acceptable/□unacceptable. (5) A bill shows: Pay to ABC Co. the sum of one thousand US dollars drawn under L/C No issued by XYZ Bank New York dated on 15 August 200X. X X Chapter2. Instruments

A bill shows: Pay to ABC Co. the sum of one thousand US dollars and charge\debit same to applicant’s account maintained with you. It is □acceptable/□unacceptable. (5) A bill shows: Pay to ABC Co. the sum of one thousand US dollars drawn under L/C No issued by XYZ Bank New York dated on 15 August 200X. X. X. Chapter2. Instruments.")

107

④ Tenor 付款期限

109

“算尾不算头;月为日历月,月之同日为到期日,无同日即月之末日付款;假日顺延 。”

到期日计算口诀 “算尾不算头;月为日历月,月之同日为到期日,无同日即月之末日付款;假日顺延 。” Chapter2. Instruments

110

a.“At ____ days after sight/date”

At 60 days sight, acceptance date is 15, May. 16, May 31, May,16 days; 1, June 30, June,30 days; 60-46=14 the maturity date is 14, July. Chapter2. Instruments

111

b.“after _____month(s)”

①At one month after 15 December one month 15 December 15th,January ② At one month after 31 January one month 31,January 28,February Chapter2. Instruments

112

⑦Name or business entity of the payee 收款人名称

1.Restrictive Order: this bill can not be transferred to any other person.限制性抬头 Pay to xxx only/not transferable 2.Demonstrative Order: this bill can be transferred to an other person by endorsement.指示性抬头 Pay to the order of xxx/ pay to xxx or order 3.Payable to Bearer: this bill can be transferred to an other person by delivery.来人抬头 Pay to bearer/pay to xxx or bearer Chapter2. Instruments

113

Additional Form see p33-35 Pay this first bill of exchange (second being unpaid)付一不付二 Referee in Case of Need需要时的受托处理人 Place of Payment 付款地点 Interest and interest rate 利息与利率 Currency 用其他货币付款 Notice of Dishonor Excused 免作退票通知或放弃拒绝证书 Without Recourse 无追索权 Limit of Time for Presentation 提示期限 Chapter2. Instruments

114

三、Acts of a bill of exchange汇票的票据行为 p21-32

Act1 Issuance出票 Act2 Endorsement背书 Act3 Presentation提示 Act4 Acceptance承兑 Act5 Payment: The act of paying /money paid付款 Act6 Dishonor拒付 Act7 Protest拒绝证书 Act8 Notice of Dishonor退票通知 Act9 Right of recourse追索权 Act10 Acceptance for Honor参加承兑 Act11 Guarantee/Aval保证 Act12 Discounting 贴现 Chapter2. Instruments

115

The general procedure of a bill of exchange

116

Act1 Issuance出票 drawer出票人 drawee Payee 收款人 payer 付款人 step 1: draw

issue step2: deliver Present for acceptance drawee Payee 收款人 Present for payment payer 付款人 Chapter2. Instruments

117

Act1 Issuance: act of giving out bill of exchange出票(p21)

Please issue a bill of exchange in accordance with the following conditions and terms, Sum: USD 47,259.00 Place of issue: Shanghai. Date of issue: 20 April, 200- Tenor: at 30 days after sight Drawer: BETERFORD DEVELOPMENT CO., LTD......Rd.,Shanghai China. Drawee: BANK OF SAIPAN,.....Rd.,Tokyo,Japan Payee: HUADONG EXPORT AND IMPORT CO., LTD....Rd,Shanghai China and make correct operation and actions Chapter2. Instruments

118

Exchange for_________ ________,________

DRAFT No Exchange for_________ ________,________ At________after sight of this FIRST of Exchange (Second of Exchange is unpaid) Pay to __________________________________ ________________________________________ The sum of ______________________________ To _______________ For __________________ (signature) USD 47,259.00 Shanghai 20 April, 200- 30 days the order of HUADONG EXPORT AND IMPORT CO., LTD....Rd,Shanghai China US Dollars Forty Seven Thousand Two Hundred Fifty Nine Only BETERFORD DEVELOPMENT CO., LTD Rd.,Shanghai China. BANK OF SAIPAN, .....Rd.,Tokyo,Japan

Pay to __________________________________. ________________________________________. The sum of ______________________________. To _______________ For __________________. (signature) USD 47, Shanghai. 20 April, days. the order of HUADONG EXPORT AND IMPORT CO., LTD....Rd,Shanghai China. US Dollars Forty Seven Thousand Two Hundred Fifty Nine Only. BETERFORD DEVELOPMENT CO., LTD Rd.,Shanghai China. BANK OF SAIPAN, .....Rd.,Tokyo,Japan.")

119

Act2 Endorsement: sign one’s name on the back of the bill, check and so on背书

Endorser has to sign on the back of the bill Made for the whole amount of the draft 背书指在票据背面或粘单上记载相关事项并签章的票据行为。 Chapter2. Instruments

120

Differences of 5 kinds of endorsement

121

If the payee of the Draft wants to negotiate the bill to BANK OF HONGKONG, please make a restrictive endorsement for it. Chapter2. Instruments

122

Pay to BANK OF HONGKONG Only For HUADONG EXPORT AND IMPORT CO., LTD

(signature) Chapter2. Instruments

Chapter2. Instruments.")

123

Act3 Presentment 提示 Sight bill Present for payment in legal time limit

提示是持票人对付款人现实地出示汇票,要求其承兑或者付款的法律行为。分为提示承兑、提示付款 Sight bill Present for payment in legal time limit Usance bill Present for acceptance in legal time limit Present for payment at maturity

124

Act4 Acceptance承兑 Acceptor engages, by signing his name across the face of the bill that he will pay when it falls due. So presentment for acceptance is legally necessary to fix the maturity date of a draft payable after sight. 承兑是指经持票人提示,付款人同意按出票人指示支付票额的行为。 Chapter2. Instruments

125

(1)一般承兑(General Acceptance)。 毫无保留地同意,不附加任何条件

承兑的类型: (1)一般承兑(General Acceptance)。 毫无保留地同意,不附加任何条件 (2)限制性承兑(Qualified Acceptance)。 对该汇票另加条款而对该票之效力有所影响 Chapter2. Instruments

一般承兑(General Acceptance)。 毫无保留地同意,不附加任何条件. (2)限制性承兑(Qualified Acceptance)。 对该汇票另加条款而对该票之效力有所影响. Chapter2. Instruments.")

126

Valid acceptance requires

一般承兑 Accepted Dated For A Co., Place (Signature) Chapter2. Instruments

Chapter2. Instruments.")

127

Qualified Acceptance Conditional acceptance有条件承兑 Partial acceptance

部分承兑 Qualified Acceptance Local acceptance 限定地点承兑 Qualified acceptance as to time限定时间承兑 Chapter2. Instruments

128

Conditional acceptance有条件承兑

Accepted 1st June,200* Payable on delivery of B/L For A Co., London (Signature) Chapter2. Instruments

Chapter2. Instruments.")

129

Partial acceptance部分承兑

Accepted 1st June,200* Payable for amount of GBP only For A Co., London (Signature) Chapter2. Instruments

Chapter2. Instruments.")

130

Local acceptance限定地点承兑

Accepted 1st June,200* Payable at the Hambros Bank and there only For A Co., London (Signature) Chapter2. Instruments

Chapter2. Instruments.")

131

Qualified acceptance as to time限定时间承兑

Accepted 1st June,200* Payable at 6 months after date For A Co., London (Signature) Chapter2. Instruments

Chapter2. Instruments.")

132

If the Drawee agree to accept the bill when he was presented on5 JUNE,200-, please make an acceptance for him. Chapter2. Instruments

133

Accepted 5 JUNE,200- For BANK OF SAIPAN,Tokyo (signature) Chapter2. Instruments

Chapter2. Instruments")

134

Act5 Payment: The act of paying /money paid付款

汇票到期时,持票人向付款人或承兑人提示付款,经其正当付款后,汇票即被解除责任 Chapter2. Instruments

135

Act6 Dishonor拒付 Act of dishonor is a failure or refusal to make acceptance on or payment of a draft when presented. a usance draft to present for acceptance Dishonor for acceptance Dishonor for payment A sight draft: legal limit A usance draft: on due date Chapter2. Instruments

136

Act7 Protest拒绝证书 Notary Public Drawee Authorized person 2.Dishonor

是由拒付地点的法定公证人作出证明拒付事实的文件。 1.presented for acceptance presented for payment Notary Public Authorized person Drawee 2.Dishonor 3.Sealed written statement——Protest Holder Chapter2. Instruments

137

Act8 Notice of dishonor退票通知

汇票一旦遭到拒付或拒绝承兑,持票人应及早通知汇票债务人。但这一行为并不具备法律效力

138

Act9 Right of recourse追索权

追索是指持票人在票据被拒付时向其前手请求偿还票据金额及其他法定款项的行为。 法律上称追索权 Chapter2. Instruments

139

Act9 Right of recourse追索权

行使追索权的三个条件: 条件1:须在规定的合理时间内向付款人提示汇票,未经提示,持票人不能对其前手追索 条件2:持票人须在退票后的次日,将退票事实通知其前手,后者再通知其前手,直到出票人 条件3:须在退票后的一个营业日内,持票人须请公证人做成拒绝证书 Chapter2. Instruments

140

Act10 Acceptance for Honor参加承兑

是指汇票遭到拒绝承兑而退票时,非汇票债务人在得到持票人同意的情况下,参加承兑已遭拒绝承兑的汇票的一种附属票据行为。其目的是为维护汇票上的某一当事人或关系人的信誉,防止追索权的行使施及该人。 Chapter2. Instruments

141

ACCEPTED FOR HONOR OF B COMPANY JULY 26, 2006 FOR K COMPANY, London

(SIGNED) Chapter2. Instruments

Chapter2. Instruments.")

142

Act11 Guarantee/Aval保证 Act of guarantee is performed by a third party called guarantor, who engages that the bill will be paid on presentation if it is a sight bill or accepted on presentation and paid at maturity if it is a time bill. 是指保证人为担保票据债务的履行,以负担同一票据债务内容为目的而作出的一种附属票据行为

143

Act12 Discounting 贴现 A bill of exchange is to sell a time bill already accepted by the drawee but not yet fallen due to a financial institution at a price less than its face value. 贴现是一种票据转让方式,是指持票人在需要资金时,将其持有的商业汇票,经过背书转让给银行,银行从票面金额中扣除贴现利息后,将余款支付给申请贴现人的票据行为

144

四、Types of bill of exchange汇票的种类

①Banker’s draft or bank draft银行汇票 ②Trade bill商业汇票 ③Trader’s acceptance bill商业承兑汇票 ④Banker’s acceptance bill银行承兑汇票 ⑤Sight bill即期汇票 ⑥Time bill远期汇票 ⑦Direct bill直接汇票:承兑地与付款地相同 ⑧Indirect bill间接汇票:付款地与承兑地不同 ⑨Inland bill国内汇票 ⑩Foreign bill外国汇票 ⑪Local currency bill本币汇票 ⑫Foreign currency bill外币汇票

145

小结 汇票的定义 汇票的8要素 汇票的12种票据行为 汇票的种类

课后作业:完善课堂上制作的汇票及各种票据行为,预习本票,注意比较本票与汇票的差别。 Chapter2. Instruments

146

On demand we promise to pay to the order of bearer

Promissory Note for USD1, Boston, 4th, June,2002 On demand we promise to pay to the order of bearer the sum of ONE THOUSAND US DOLLARS Payable at Boston For: First National Bank of Boston __________________________ Authorized Signature(s)

")

147

Maker and payer are the same person

Promissory Note New York, April 1, 2001 For USD99,999.00 On the 20th June 2001 fixed by the promissory note we promise to pay BA the sum Of ninety-nine thousand nine hundred and ninety-nine US Dollars only For and on behalf of DC (signed) Promissory Note we promise to pay Maker and payer are the same person Chapter2. Instruments

Promissory Note. we promise to pay. Maker and payer. are the same person. Chapter2. Instruments.")

148

(2)Promissory note 本票 Chapter2. Instruments

Promissory note 本票 Chapter2. Instruments")

149

1) Definition of promissory note本票的定义

A promissory note is unconditional promise in writing , made by one person(maker) to another(payee),signed by the maker,engaging to pay on demand or at fixed or determinable future time , a sum certain in money to or to the order of a specified person or to bearer. 本票是一人(制票人)向另一人(收款人)签发的,保证即期或定期或在可以确定的将来时间,对某人或其指定人或执票人支付一定金额的无条件书面承诺 Chapter2. Instruments

to another(payee),signed by the maker,engaging to pay on demand or at fixed or determinable future time , a sum certain in money to or to the order of a specified person or to bearer. 本票是一人(制票人)向另一人(收款人)签发的,保证即期或定期或在可以确定的将来时间,对某人或其指定人或执票人支付一定金额的无条件书面承诺. Chapter2. Instruments.")

150

EXHIBIT-2 Maker and payer are the same person

Promissory Note New York, April 1, 2001 For USD99,999.00 On the 20th June 2001 fixed by the promissory note we promise to pay BA the sum Of ninety-nine thousand nine hundred and ninety-nine US Dollars only For and on behalf of DC (signed) Promissory Note we promise to pay Maker and payer are the same person

Promissory Note. we promise to pay. Maker and payer. are the same person.")

151

2) Characteristics of promissory note

①It is an in writing ② Two basic parties: ③ There is no on it ④ The maker is the ⑤ Promissory notes other than those issued by banks are not very widely used in modern commercial transactions. Bearer promissory notes payable on demand and issued by banks are equivalent to bank notes of large denomination(面额) , which may cause inflation and are prohibited by the government in may countries. unconditional promise maker, payee Maker has signed his name on the face of it acceptance primarily liable party

, which may cause inflation and are prohibited by the government in may countries. unconditional promise. maker, payee. Maker has signed his. name on the face of it. acceptance. primarily liable party.")

152

EXHIBIT-1 ① ⑥ ⑦ ② ⑤ ③ Promissory Note for New York ________ At* * * * *sight we promise to pay to___________________________ ______________________________________________________ the sum of__________________________________________ ______________________________________________Payable at _____________ For Authorized Signature(s) ⑧ ⑦ ④

⑧ ⑦ ④.")

153

3) Essentials to a promissory note本票的要素

①The words clearly indicated ② An to pay ③ Name of the or his order ④ ’s signature ⑤ of issue ⑥ of payment ⑦ A of money ⑧ of payment “promissory note” unconditional promise payee Maker Place and date Period certain amount Place Chapter2. Instruments

154

Chapter2. Instruments On demand we promise to pay to

Promissory Note for USD1, Boston, 4th, June,2002 On demand we promise to pay to the order of bearer the sum of ONE THOUSAND US DOLLARS Payable at Boston For: First National Bank of Boston __________________________ Authorized Signature(s) Chapter2. Instruments

Chapter2. Instruments.")

155

4) Difference between a promissory note and a bill of exchange

①A promissory note is a promise to pay, whereas a bill of exchange is an order to pay ② There are only two parties to a promissory note, namely the maker and the payee (or the holder in the case of a bearer note), whereas there are three parties to a bill of exchange, namely the drawer, the drawee and the payee Chapter2. Instruments

, whereas there are three parties to a bill of exchange, namely the drawer, the drawee and the payee. Chapter2. Instruments.")

156

③ The maker is primarily liable on a promissory note, whereas the drawer is primarily liable, if it is a sight bill, and the acceptor becomes primarily liable, if it is a time bill ④ When issued, a promissory note has an original note only, whereas a bill of exchange may be either a sole bill or a bill in a set. duplicate Chapter2. Instruments

157

Promissory note Bill of exchange A promise to pay An order to pay Two basic parties Three basic parties Maker is primarily liable Sight bill: drawer is primarily liable Accepted usance bill: acceptor is primarily liable An original note In a set or a sole

158

Exercises (一)Compare the following promissory notes.

1、Banker’s promissory note Promissory Note for USD1, Boston, 4th, June,2002 On demand we promise to pay to the order of bearer the sum of ONE THOUSAND US DOLLARS Payable at Boston For: First National Bank of Boston __________________________ Authorized Signature(s) Haverty Furniture Companies USD100, Atlanta 6,Otc. 2002 At SEVENTY DAYS AFTER DATE we promise to pay to the order of bearer the sum of ONE HUNDDRED THOUSAND US DOLLARS Payable AT FULTON NATIONAL BANK, MAIN OFFICE, ATLANTA, GEORGIA HAVERTY FURNITURE CO. __________________________ Authorized Signature(s)

Haverty Furniture Companies. USD100, Atlanta 6,Otc At SEVENTY DAYS AFTER DATE we promise to pay to. the order of bearer. the sum of ONE HUNDDRED THOUSAND US DOLLARS. Payable AT FULTON NATIONAL BANK, MAIN OFFICE, ATLANTA, GEORGIA. HAVERTY FURNITURE CO. __________________________. Authorized Signature(s)")

159

The word “promise note” Unconditional promise to pay Payee Maker

BANKER’S PROMISSORY NOTE TRADER’S PROMISSORY NOTE The word “promise note” Unconditional promise to pay Payee Maker Date and place of issue Tenor Amount Place of payment Presentation Primarily liability

160

(二)Issue a promissory note

⑴Amount £3,026.00 ⑵Date and place of issue 8/August/2003,Guangzhou, China ⑶Tenor At 90 days after date ⑷Maker Guangdong Imp. & Exp. Co., Guangzhou ⑸Payee Chemicals Import & Export Company London

161

Chapter2. Instruments Promissory Note for______________________

(Amount in figure) ________, ______________,200_ (Place and date of issue) (Name of month in letter) On _________________________against this promise note I( we) promise to pay to ________________________________________________________or order the sum of____________________________________________________________ FOR VALUE RECEIVED________________________________________________ Payable at__________________ _______________ Signature(s) and full address of maker Chapter2. Instruments

________, ______________,200_. (Place and date of issue) (Name of month in letter) On _________________________against this promise note I( we) promise to. pay to ________________________________________________________or order. the sum of____________________________________________________________. FOR VALUE RECEIVED________________________________________________. Payable at__________________. _______________. Signature(s) and full address of maker. Chapter2. Instruments.")

162

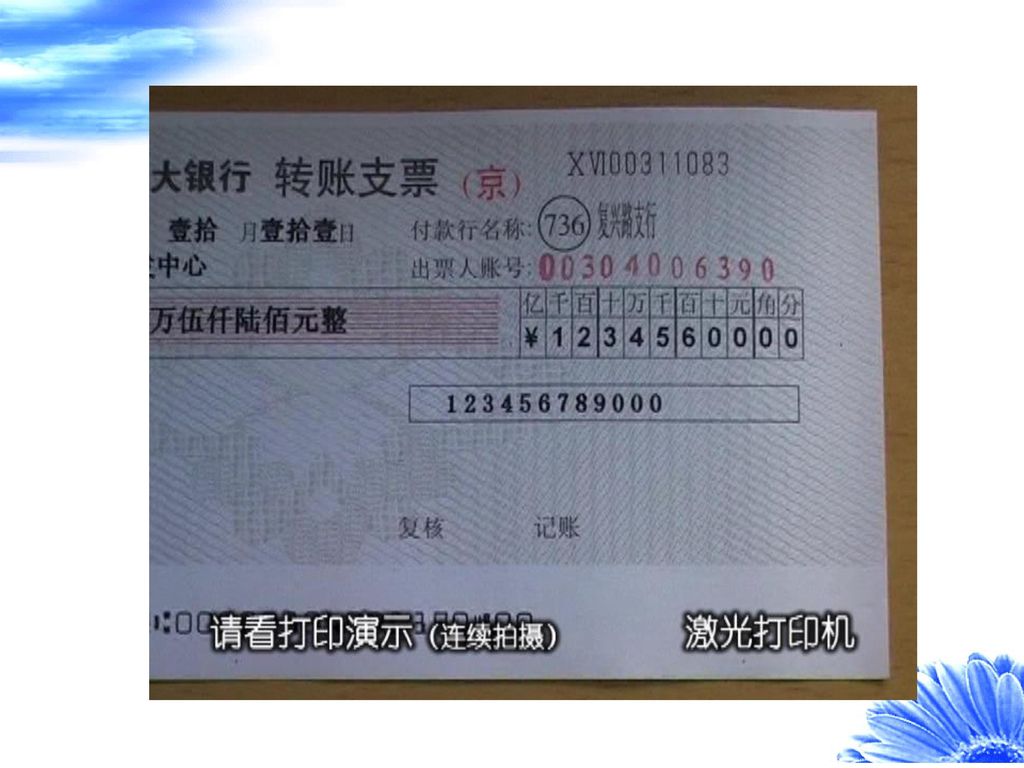

(3) Cheque/Check 支票 Chapter2. Instruments

Cheque/Check 支票 Chapter2. Instruments")

163

支票存根

165

1)Definition of check支票的定义

A check is an unconditional order in writing, addressed by the customer(the drawer)to a bank(the drawee)signed by that customer authorizing the bank to pay on demand a specified sum of money to or to the order of a named person or to bearer (the payee). 支票是出票人签发的,委托办理支票存款业务的银行或者其他金融机构在见票时无条件支付确定的金额给收款人或者持票人的票据。

to a bank(the drawee)signed by that customer authorizing the bank to pay on demand a specified sum of money to or to the order of a named person or to bearer (the payee). 支票是出票人签发的,委托办理支票存款业务的银行或者其他金融机构在见票时无条件支付确定的金额给收款人或者持票人的票据。")

166

Features of a check支票的特点

unconditional ①A check must be ② A check must be drawn on a ③ A must be written on a check, which should be signed by or per procurement for the drawer ④ The date of a check is not essential in that it can be antedated, post-dated or dated on a non-business day ⑤ The payee may be bearer, a specified person or his order. bank sum certain in money Antedated 比实际早的日期 post-dated 把日期填迟

167

3)Essentials to a check支票的要素

①The words “ ” clearly indicated ② An in writing ③ Name of the ④ ’s signature ⑤ of issue ⑥Address of the ⑦ A in money ⑧ Name of check unconditional order paying bank Drawer Place and date paying bank sum certain payee

168

A banker’s duty to dishonor checks

①on countermanding of payment by the customer—commonly known as “stop” 客户发出止付通知 ② on receiving notice that the customer has died or dissolved 死亡或解散 ③ on receiving notice of bankruptcy or liquidation of the customer. 破产或清算 ④ On receiving order that is made against the customer ⑤ on receiving notice of mental disorder of the customer. 精神失常 ⑥on receiving a garnishee order against the customer’s account ⑦on receiving a court order freezing the customer’s account 法院指令 冻结客户账户 The banker is obliged to honor a customer’s checks up to the amount of his credit balance or available overdraft limit. The banker’s duty to honor the check end:

169

Countermand of payment支票的止付 撤回 取消

Countermand of payment denotes the cancellation by the customer(the drawer) of his mandate(指令 )to the drawee bank or paying bank of the check, but in order to be effective the countermand must actually come to that bank’s notice. Mere constructive countermand, such as the bank is supposed to be in a position to learn of the stop payment, is not enough. The drawer is the only person who can instruct the drawee bank to stop payment on a particular check. 书面的止付通知书 出票人有权发出止付通知

of his mandate(指令 )to the drawee bank or paying bank of the check, but in order to be effective the countermand must actually come to that bank’s notice. Mere constructive countermand, such as the bank is supposed to be in a position to learn of the stop payment, is not enough. The drawer is the only person who can instruct the drawee bank to stop payment on a particular check. 书面的止付通知书. 出票人有权发出止付通知.")

170

Reasons Signature differs Words and Figures differs

Amount in words requires drawer's conformation Insufficient fund Amount required in words Orders not to pay Irregularly drawn Post-dated Out of date or stale check Payee's endorsement required Refer to drawer Material Alterations to be confirmed by drawer

171

3) Kinds of check支票的种类 Kinds Writing Characteristics Order check

┌ the order of sb. Pay to┼ sb. or order └ sb. Endorsement and delivery Bearer check Pay bearer Delivery Crossed check General crossing One with two parallel lines drawn across it Payable through any banker Special crossing Payable through a bank mentioned in the check Certified check Certified Check Certified by the paying banker Banker’s check Banker's Check Drawer and drawee are bankers

172

Crossed check划线支票 A crossing is in effect an instruction to the paying bank from the drawer or holder to pay the fund to a bank only. Hence, such checks will not be paid over the counter of the paying bank and must be presented for payment by a collecting bank. 在支票正面划有两条平行线的支票称为划线支票。划线后支票只能委托银行转账,持票人不能提现。划线是一种附属的支票行为,由出票人、背书人或持票人划上,目的在于防止支票丢失和被盗时被人冒领 Chapter2. Instruments

173

1. General crossing普通划线 Where a check bears across its face an addition of: The words “ and company”, or any abbreviation thereof, between two parallel transverse lines, either with or without the words “not negotiable” Two parallel transverse lines simply, either with or without the words “not negotiable”, that addition constitutes a crossing, and the check is crossed generally. The effect of a general crossing is to make the check payable only through any another banker( it must be deposit into a bank account for clearing)

")

174

BCD Bank for collection

Examples-1 ABC Bank ABC Bank a/c payee ABC Bank BCD Bank for collection Chapter2. Instruments

175

2. Special crossing特别划线 Where a check bears across its face an addition of the name of a bank, either with or without the two parallel transverse lines, that addition constitutes a special crossing. If a check is crossed specially, only the bank mentioned in the check can received payment from the drawee bank.划线后支票只能委托银行转账,持票人不能提现 目的在于防止支票丢失和被盗时被人冒领

176

___________________________ For: B Company

Examples-2 EAST ASIA BANK Hongkong Branch Pay to the order of A Company Hong Kong Dollars One Thousand $1,000.00 ___________________________ For: B Company John Smith ABC Bank Limited A Company’s bank is A Bank, do you know how to collect the above check?

177

保付支票certified cheque a check containing certification that the person who issued the check has sufficient funds on deposit to cover payment 保付支票 为了避免出票人开空头支票,收款人或持票人可以要求付款行在支票上加盖“保付”印记,以保证到时一定能得到银行付款。 支票受款人取得支票后往往并不立即向付款银行提现,但为确定支票付款的真实性,或为增强支票的流通能力,就将支票转往付款银行,请求保付。支票一经付款银行保付,付款责任就由保付银行承担,发票人和背书人等均不再负责任。这种支票与银行本票性质基本相同。同时,银行保付的支票金额必须在存款余额或透支限额以内,如有超过,法院将对保付银行处以罚款。此外,银行在保付支票的同时,应将支票所载金额由存款帐户内划出,转入保付帐户,以保证能按约付款。

178

保付支票certified cheque 记载有付款人书写的“保付”、“照付”或其他同义字样的支票。保付支票源于美国。支票保付与汇票承兑相类似,但汇票经承兑后,其他债务人的责任不能免除;而支票经保付后,发票人与其他债务人的责任均予免除,保付人成为支票上唯一的债务人。支票保付与票据的保证有类似之处,但也有差异:(1)保付只能由支票付款人作出,而票据保证则可由在票据上签名的人或第三人作出。(2)支票经保付后,持票人不能再行使追索权;而票据经保证后,持票人仍可行使追索权。(3)支票的保付应由当事人另行作出约定,付款人不承担法定的保付义务,即保付须经付款人同意,而且付款人同意保付后,应当在支票上记载“保付”、“照付”或者其他同义字样,并签名。(4)付款人保付支票后,成为支票上的主债务人,负有绝对付款的义务,即不论发票人在付款人处有无资金,不论持票人是否在法定提示期间内作出提示,也不论发票人是否撤回其付款委托,付款人均须付款。保付支票的发票人和背书人因保付而免除责任,即使付款人拒绝付款,持票人也不能向发票人和背书人行使追索权。保付支票的持票人取得绝对的付款请求权。

保付只能由支票付款人作出,而票据保证则可由在票据上签名的人或第三人作出。(2)支票经保付后,持票人不能再行使追索权;而票据经保证后,持票人仍可行使追索权。(3)支票的保付应由当事人另行作出约定,付款人不承担法定的保付义务,即保付须经付款人同意,而且付款人同意保付后,应当在支票上记载 保付 、 照付 或者其他同义字样,并签名。(4)付款人保付支票后,成为支票上的主债务人,负有绝对付款的义务,即不论发票人在付款人处有无资金,不论持票人是否在法定提示期间内作出提示,也不论发票人是否撤回其付款委托,付款人均须付款。保付支票的发票人和背书人因保付而免除责任,即使付款人拒绝付款,持票人也不能向发票人和背书人行使追索权。保付支票的持票人取得绝对的付款请求权。")

179

支票遗失的案例 案情简介 1990年5月3日,某机械有限责任公司职工许某向该厂财务部门领取了盖有银行预留印鉴的空白转帐支票一张,号码为001403,准备用于采购生产用品,不慎在途中遗失。该厂即向开户银行办理挂失手续,因按规定不能办理挂失而未遂。 5月11日,某机械有限责任公司在当地日报上刊登了支票遗失启事,声明遗失的001403号空白转帐支票作废。 Chapter2. Instruments

180

支票遗失的案例 案情简介 同年8月8日,自称“付军”的人持该空白转帐支票到某微型电机有限责任公司,以某机械有限责任公司名义购买电器,并出示了名片和介绍信。某微型电机有限责任公司财务人员未严格审证,就在该空白转帐支票上填写了收款单位、金额、用途。同日,“付军”即将价值8000元的电器提走。 Chapter2. Instruments

181

支票遗失的案例 案情简介 8月13日,某微型电机有限责任公司持该转帐支票到某机械有限责任公司的开户银行去兑付,银行发现某机械有限责任公司的存款不足,予以退票,并按规定对某机械有限责任公司作出罚款处理。某微型电机有限责任公司遂与某机械有限责任公司交涉,要求该厂承担货款。但某机械有限责任公司以遗失的空白转帐支票已登报声明作废为理由,拒绝支付货款。 Chapter2. Instruments

182

支票遗失的案例 案情简介 为此,某微型电机有限责任公司于1990年8月28日向人民法院提起诉讼,称:某机械有限责任公司违反支票管理规定,支票遗失后被他人冒用,造成我厂经济损失8000元,要求某机械有限责任公司予以赔偿。 某机械有限责任公司辩称:向原告购物的空白转帐支票确系我厂签发,但该空白转帐支票遗失后,我厂已登报声明该空白转帐支票作废。原告被自称“付军”的人诈骗价值8000元的电器,与我厂无关,请求法院判决驳回原告的诉讼请求。 Chapter2. Instruments

183

支票遗失的案例分析 Chapter2. Instruments

在本案中,某机械有限责任公司之所以应承担赔偿责任,原因有二: 1、违反了票据管理使用规定。 支票是资金结算的依据,应按支票管理的有关规定正确使用。《中华人民共和国票据法》第八十八条规定:“支票的出票人所签发的支票金额不得超过其付款时在付款人处实有的存款金额。 出票人签发的支票金额超过其付款时在付款人处实有的存款金额的,为空头支票。禁止签发空头支票。” 某机械有限责任公司签发空白转帐支票,且银行存款不足,其行为是违反支票管理使用的有关规定的。该001403号空白转帐支票被他人冒用,造成原告8000元的经济损失,由此造成某微型电机有限责任公司的经济损失,某机械有限责任公司应负赔偿责任。 Chapter2. Instruments

184

支票遗失的案例分析 2、登报声明支票作废的作为是一种单方法律行为,对第三人不具有法律拘束力。《银行结算办法》第16条第1款第(九)项规定:“已签发的转帐支票遗失,银行不受理挂失,可请求收款人协助防范。”这个规定充分说明,在转帐支票遗失的情况下,签发人只有向特定人即支票上记明的收款人请求协助防范,才可能起到防止损害发生的作用。除此之外,向不特定人声明,就不具有这种作用。因此,因支票遗失造成他人的经济损失,不能免除其赔偿责任。《银行结算办法》第21条还明确规定,票据丢失造成资金损失的,应由其自行负责。这说明,登报声明遗失的支票作废的行为,不产生对外不负责任的后果。 此外,某微型电机有限责任公司“付军” 审证不严,故在这起纠纷中也有一定责任:未严格审证,擅自在空白转帐支票上填写收款单位、金额、用途,也有一定过错,应承担一定责任,承担部分经济损失 Chapter2. Instruments

项规定: 已签发的转帐支票遗失,银行不受理挂失,可请求收款人协助防范。 这个规定充分说明,在转帐支票遗失的情况下,签发人只有向特定人即支票上记明的收款人请求协助防范,才可能起到防止损害发生的作用。除此之外,向不特定人声明,就不具有这种作用。因此,因支票遗失造成他人的经济损失,不能免除其赔偿责任。《银行结算办法》第21条还明确规定,票据丢失造成资金损失的,应由其自行负责。这说明,登报声明遗失的支票作废的行为,不产生对外不负责任的后果。 此外,某微型电机有限责任公司 付军 审证不严,故在这起纠纷中也有一定责任:未严格审证,擅自在空白转帐支票上填写收款单位、金额、用途,也有一定过错,应承担一定责任,承担部分经济损失. Chapter2. Instruments.")

185

Difference between a check and a bill of exchange

A bill of exchange may be payable at sight or at future day,check must be paid at sight A bill of exchange may be drawn upon any person, whereas a check must be drawn upon a banker. Unless a bill is payable on demand, it is usually accepted, whereupon the acceptor is the primarily liable party. A check need not be accepted for it is payable only on demand and the drawer is the party primarily liable.

186

Difference between a check and a bill of exchange

4. A bill must be presented for payment when due, or else the drawer will be discharged. A check must be presented for payment within a reasonable time or within a certain time. Such as 30 days according to the regulations of the country concerned. The drawer of a check is not discharged even though it has not been presented for payment within the stipulated time unless the delay in presentation incurs losses to the drawer. 5. bill of exchange can be issue by set, but check can issue one piece

187

Sight bill;Usance bill Should be presented for payment when due

Check Bill of exchange One piece Can be issued by set Drawn on a banker Drawn on any person Sight check Sight bill;Usance bill Within a certain time, Such as 30 days Should be presented for payment when due No acceptance; Drawer is primarily liable for payment Sight bill: drawer is primarily liable for payment Accepted usance bill: acceptor is primarily liable for payment

188

Exercises (一)Examine the following check. Chapter2. Instruments

Check No New York, 16th, Dec., 2003 Pay to the order of Toyota Company the sum of five thousand US dollars To Bank of New York For BBB Corp., New Yor New York ___________ Authorized Signature(s) Chapter2. Instruments

Chapter2. Instruments.")

189

The word “check” Unconditional order to pay Date and place of issue Amount Drawer Payee Drawee No. of the check Presentation The relationship between “bank of New York” and “BBB Corp., New York”

190

(二)Issue a check ⑴Drawer Thames Enterprises Ltd., London ⑵Drawee

The National Westminster Bank Ltd., London ⑶Payee Philips Hong Kong ⑷Date and place of issue 07/01/2001,London ⑸Amount GBP79,014 Chapter2. Instruments

191

National Westminster Bank Ltd., London

Check No _______,_____, 200_ National Westminster Bank Ltd., London Pay to the order of ___________________________________ the sum of _____________________________________ GBP For and on behalf of ___________ Authorized Signature(s) Chapter2. Instruments

Chapter2. Instruments.")

192

A bill of exchange shows as follows:

Chapter2. Instruments

193

The above bill was accepted on 12 August by B bank ,HongKong.

(1)Payment in due course for such bill means the sum of paid by at after maturity, i.e to the holder, i.e in good faith and without notice that title to bill is defective. (2)If C Co. Presented the bill on 8 Oct. for payment,B Bank,HongKong Paid it accordingly,it 口 is/ 口 isn't payment in due course. (3)If C Co. lost the bill which was picked up by D who has forged C Co's endorsement and it for payment on 10 Oct.,B Bank,HongKong did not check endorsement and paid D accordingly,it 口 is/ 口 isn't payment in due course. Chapter2. Instruments

Payment in due course for such bill means the sum of. paid by at after maturity, i.e. to the holder, i.e. in good faith and without notice that. title to bill is defective. (2)If C Co. Presented the bill on 8 Oct. for payment,B Bank,HongKong Paid it accordingly,it 口 is/ 口 isn t payment in due course. (3)If C Co. lost the bill which was picked up by D who has forged C Co s endorsement and it for payment on 10 Oct.,B Bank,HongKong did not check endorsement and paid D accordingly,it 口 is/ 口 isn t payment in due course. Chapter2. Instruments.")

194

(4)If C Co. lost the bill which had been endorseed in blank, and then it was picked up by D who presented it for payment. B Bank,HongKong without notice that D had picked up the bill, paid him on 10 Oct., it 口 is/ 口 isn't payment in due course. (5)If B Bank,HongKong was called by telephone that C Co.lost the bill B Bank still paid it to D on 10 Oct., it 口 is/ 口 isn't payment in due course. Chapter2. Instruments

If B Bank,HongKong was called by telephone that C Co.lost the bill B Bank still paid it to D on 10 Oct., it 口 is/ 口 isn t payment in due course. Chapter2. Instruments.")

195

(1)HKD10,000.00 B Bank , HongKong 9 Oct. C Co. C Co’s (2)× (3)× (4)×

(5)× Chapter2. Instruments

× Chapter2. Instruments.")

196

Chapter 3. Remittance 汇款 Chapter3. Remittance

197

In this chapter, you will learn

1)Remittance and reverse remittance methods 2)parties and procedures of remittance 3) Advantages and disadvantages of remittance 4)Practice of remittance (reimbursement)偿还 5) The function of remittance in international trade Chapter3. Remittance

Remittance and reverse remittance methods. 2)parties and procedures of remittance. 3) Advantages and disadvantages of remittance. 4)Practice of remittance (reimbursement)偿还. 5) The function of remittance in international trade. Chapter3. Remittance.")

198

Remittance and reverse remittance

顺汇 逆汇 Remittance and reverse remittance The reverse remittance is that the funds flow in a contrary direction to the payment instructions transmitted therefore 由债权人以开出汇票的方式托银行向债务人索取款项 The remittance is that the funds flow in a favorable direction to the payment instructions(指示) transmitted therefore 由债务人或进口商主动将款项交给银行汇交债权人或出口商 Chapter3. Remittance

transmitted therefore. 由债务人或进口商主动将款项交给银行汇交债权人或出口商. Chapter3. Remittance.")

199

Funds flow Payment instruction Remittance Payee(Beneficiary) Payer

Importer’s Bank Exporter’s Bank The buyer on his own initiative remits money to the seller through a bank. 汇款属于顺汇,即汇款人主动将款项通过银行交付给收款人。

200

Funds flow Payment instruction Reverse remittance Payer

Payee(Beneficiary) Collection Letter of credit Importer’s Bank Exporter’s Bank The seller on his own initiative asks a bank to get money from the buyer. 托收、信用证属于逆汇,即收款人主动委托银行向付款人收款。

Collection. Letter of credit. Importer’s. Bank. Exporter’s. Bank. The seller on his own initiative asks a bank to get money from the buyer. 托收、信用证属于逆汇,即收款人主动委托银行向付款人收款。")

201

Definition of a international bank remittance定义

汇款人 汇出行 A client(payer) asks his bank (remitting bank), by one of the transfer methods at his option(选择) to send a sum of money to its branch or correspondent or accounting bank(paying bank) in another country and instructing the latter to pay a certain amount of money to a beneficiary. 汇入行 收款人

asks his bank (remitting bank), by one of the transfer methods at his option(选择) to send a sum of money to its branch or correspondent or accounting bank(paying bank) in another country and instructing the latter to pay a certain amount of money to a beneficiary. 汇入行. 收款人.")

202

银行接受客户的委托,使用一定的结算工具, 通过其在海外的分支机构或代理行,把款项付给 国外收款人的一种结算方式。

remitting bank remitter Standard of classification 银行接受客户的委托,使用一定的结算工具, 通过其在海外的分支机构或代理行,把款项付给 国外收款人的一种结算方式。 paying bank Payee/ beneficiary. Chapter3. Remittance

203

2)Parties concerned Remitter Payee Remitting Bank 汇出行 Paying Bank 汇入行

Who is addressed to receive the remittance. Requests his bank to remit funds to a beneficiary in a foreign currency. Entrusted by the remitting bank to pay a certain amount of money to a beneficiary. Transferring funds at the request of a remitter to its correspondent or its branch in another country and instructing the latter to pay a certain amount of money to a beneficiary. Remitting Bank 汇出行 Paying Bank 汇入行

204

Relationship between the parties

depositor、 depository bank remitter remitting bank paying remittance application form Trust business Remittance instruction/ cable/ instruments overseas branch correspondent bank accounting bank Chapter3. Remittance

205

3)Methods and procedures汇款的方式和流程

1.Telegraphic Transfer(T/T)电汇 Remitting bank transmitted instructions to paying bank by cable电报 /telex电传 /SWIFT. Chapter3. Remittance

电汇. Remitting bank transmitted instructions to paying bank by cable电报 /telex电传 /SWIFT. Chapter3. Remittance.")

206

电报或电传方式的汇款应具备下列内容: FM:(汇出行名称) TO:(汇入行名称) DATE(发电日期) TEST(密押)

OUR REF NO (汇款编号) NO ANY CHARGES FOR US(我行不负担费用) PAY (AMT) VALUE (DATE) (付款金额、利息日) TO BENEFICIARY(收款人) MESSAGE (汇款附言) ORDER (汇款人) COVER (头寸拨付) Chapter3. Remittance

NO ANY CHARGES FOR US(我行不负担费用) PAY (AMT) VALUE (DATE) (付款金额、利息日) TO. BENEFICIARY(收款人) MESSAGE (汇款附言) ORDER (汇款人) COVER (头寸拨付) Chapter3. Remittance.")

207

Diagram Remitter Beneficiary Remitting Paying Bank Bank 5. 2.T/T

4.Notify the beneficiary 5. Signed for payment 2.T/T receipt 1.T/T application 6. Funds Remitting Bank Paying Bank 3.Cable/telex/SWIFT 7.Debit advice Chapter3. Remittance

208

美元通过CHIPS电支付方式 CHIPS是纽约清算所银行间支付系统的缩写,有一百多家银行参加组成,其中12家是清算银行,它们都在联邦储备银行开立账户,作为联邦系统成员银行。每个会员银行均有ABA号码,作为参加CHIPS清算时的代号,而所属客户会有清算所发给通用认证号码,即UID号码,作为收款人(或收款行)代号。 通过CHIPS的每笔收付都由付款一方的CHIPS会员银行主动通过CHIPS终端发出付款指示,注明账户行ABA号码和收款行UID号码,经CHIPS电脑中心传递给另一家CHIPS会员银行,收在其客户的账户上。 Chapter3. Remittance

代号。 通过CHIPS的每笔收付都由付款一方的CHIPS会员银行主动通过CHIPS终端发出付款指示,注明账户行ABA号码和收款行UID号码,经CHIPS电脑中心传递给另一家CHIPS会员银行,收在其客户的账户上。 Chapter3. Remittance.")

209

2.Mail Transfer(M/T)信汇 Remitting bank transmitted instructions to paying bank by airmail of a payment order or mail advice. 支付委托书/信汇委托书 汇费相对低廉;资金汇兑速度取决于邮递速度,相对较慢;银行有机会占用客户的在途汇款资金。当今,在注重风险规避、讲求效率及投资回报的国际经济氛围中,尽管信汇的成本低廉,但其使用率仍呈下降态势

210

Diagram Remitter Beneficiary Remitting Paying Bank Bank 5. 2.M/T

4.Notify the beneficiary 5. Signed for payment 2.M/T receipt 1.M/T application 6. Funds 3.Payment order airmail advice Remitting Bank Paying Bank 7.Debit advice Chapter3. Remittance

211

3.Remittance by banker’s Demand Draft(D/D)票汇

Remitting bank draw a banker’s draft on paying bank ordering the latter to pay on demand the stated amount to the holder of the draft. 银行即期汇票 Chapter3. Remittance

212

Diagram Remitter Beneficiary Remitting Paying Bank Bank 1.D/D 6.

3.Banker’s demand draft 5.Present the draft for payment 2.Banker’s demand draft 1.D/D application 6. Funds 4.Advice of Banker’s demand draft Remitting Bank Paying Bank 7.Debit advice Chapter3. Remittance

213

Draft on Centre p112 “中心汇票”在汇款业务中的应用

①什么是中心汇票? 银行开出汇票,其付款行是在货币清算中心城市的汇票叫做中心汇票 ②为什么要用中心汇票? 不寄票根,不拨头寸,也不占用出票行资金,只需要在清算中心帐户进行帐面操作。 ③怎样使用中心汇票? Chapter3. Remittance

214

1.M/T rate =T/T-银行占用客户资金的利息 2.D/D rate =T/T-银行占用客户资金的利息

3.电汇:0.1%,每笔最低收50元人民币,最高收1000元人民币 4.信汇,票汇:0.1%,每笔最低收100元人民币,最高收1000元人民币 Chapter3. Remittance

215

4)Advantages and disadvantages

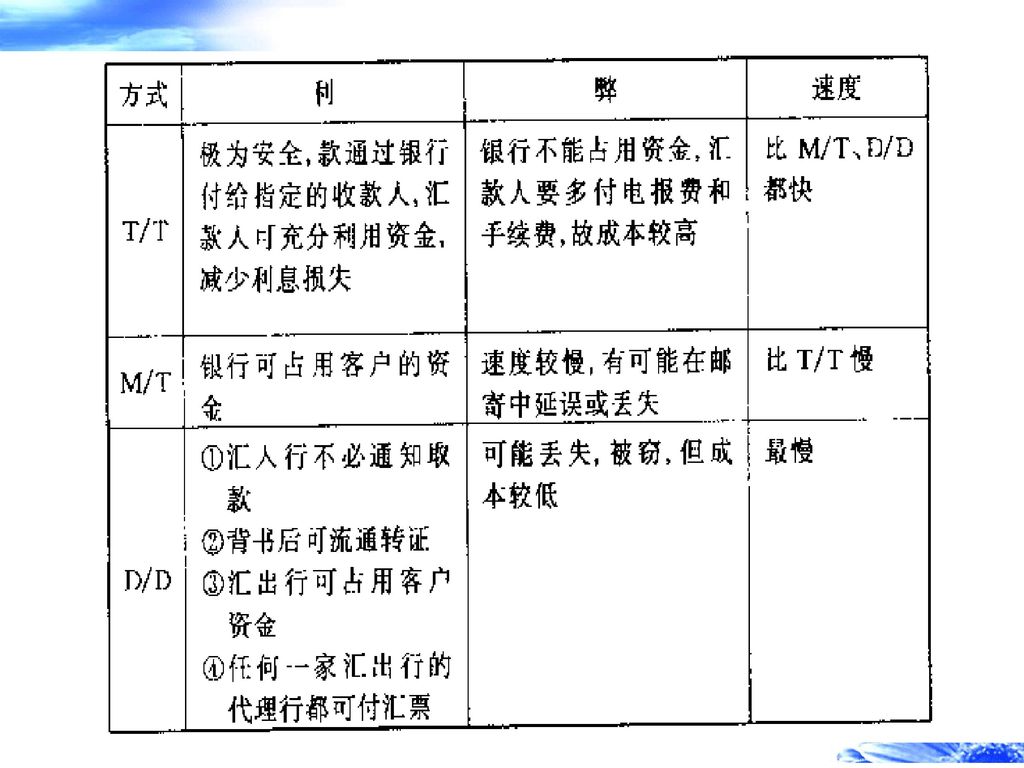

⑴D/D:Demand draft is a negotiable instrument, which can be transferred from one person to another by endorsement, so that it is more convenient in use for payment. 流通票据可背书转让 ⑵ M/T: Bank-to-bank instructions with banks responsible for making payments, so it is rather reliable;收款可靠 ⑶ T/T: Fastest way to transfer funds; Bank-to-bank instructions with banks responsible for making payments, so it is quite safe,especially when large amount is transferred. 速度最快,适用于较大金额的汇款

216

2.Disadvantages ⑴D/D: ①Remitter himself is responsible for mailing the demand draft, its transmission is slower than that of T/T and cannot serve the purpose of quick payment; 速度慢 ② It is possible for a demand draft to be lost, stolen or destroyed; 即期汇票被遗失、被窃或遭毁坏 ③ The remitting bank is reluctant to stop payment on a draft issued by itself for this would mean an act of dishonor on its part which will have an unfavorable effect on its credit-worthiness. 止付汇票将影响银行的信誉 To stop payment on lost draft is time consuming .旷日持久 Chapter3. Remittance

217

2.Disadvantages ⑵M/T: ①Mail transfer order to be delayed or lost in the post, thus causing difficulty for its payment; ② Its transmission is slower than that of T/T and cannot serve the purpose of quick payment; ③The beneficiary must await notification from the bank concerned. 资金汇兑速度取决于邮递速度,相对较慢;银行有机会占用客户的在途汇款资金。 Chapter3. Remittance

218

2.Disadvantages ⑶ T/T: ①It is more expensive as compared with M/T or D/D, but if the amount transferred is large, the interest cost which should be otherwise incurred due to time delay can be saved; ② The beneficiary must await notification (通知,通告)from the bank concerned. 由于汇票的转让流通,加大了汇票所体现的汇款资金的流动性及银行对持票人身份确认的难度, 票汇的汇兑速度取决于汇款人寄发汇票的时间及邮递速度,银行通常可占用在途汇款资金 Chapter3. Remittance

from the bank concerned. 由于汇票的转让流通,加大了汇票所体现的汇款资金的流动性及银行对持票人身份确认的难度, 票汇的汇兑速度取决于汇款人寄发汇票的时间及邮递速度,银行通常可占用在途汇款资金. Chapter3. Remittance.")

219

Summary ⑴M/T usually made by individuals for family maintenance, cash gift, etc. 生活费,礼物 ⑵ T/T is favorable to the seller, who can speed up the turnover of funds, increase the income of interests and avoid the risk of fluctuation in the exchange rate.加快资金周转,避免汇率风险 ⑶However, the seller should prevent the buyer from forcing the contractual price down under the pretext of bearing more expenses. 进口商借口支付过多的汇费而压低合同价格 Chapter3. Remittance

220

⑷ SWIFT can provides the member banks with faster, safer, cheaper, and more reliable handling of their customers’s transactions., Swiftness, reliability, safety, and inexpensiveness are major advantages of transactions by means of SWIFT messages. Chapter3. Remittance

222

Diagram Remitter Beneficiary Remitting Paying Bank Bank 5. 2.T/T

4.Notify the beneficiary 5. Signed for payment 2.T/T receipt 1.T/T application 6. Funds Remitting Bank Paying Bank 3.Cable/telex/SWIFT 7.Debit advice Chapter3. Remittance

223

Usually adopted procedures for M/T and T/T

(1)The remitter (a bank’s customer) makes out the necessary application form and gives his signed written application to his bank instructing it to issue an M/T or T/T. Indicating the beneficiary’s full name,address and the name of beneficiary’s banker (if any). This actually means that the remitter sends a written order to the remitting bank to pay t the debit of the remitter’s account or against cash deposit. (2)The remitting bank debits his customer’s account with the amount to be remitter together with its commission and expenses (if any). Chapter3. Remittance

The remitter (a bank’s customer) makes out the necessary application form and gives his signed written application to his bank instructing it to issue an M/T or T/T. Indicating the beneficiary’s full name,address and the name of beneficiary’s banker (if any). This actually means that the remitter sends a written order to the remitting bank to pay t the debit of the remitter’s account or against cash deposit. (2)The remitting bank debits his customer’s account with the amount to be remitter together with its commission and expenses (if any). Chapter3. Remittance.")

224

Usually adopted procedures for M/T and T/T

(3)The remitting bank issues a payment order to its branch or correspondent in the place where the beneficiary is domiciled.指定支付地点的 The payment order specifies the details of the payment: amount, name and address of the Beneficiary, and name of the remitter. The payment order must be authenticated with the authorized signatures of the remitting bank. Chapter3. Remittance

The remitting bank issues a payment order to its branch or correspondent in the place where the beneficiary is domiciled.指定支付地点的. The payment order specifies the details of the payment: amount, name and address of the Beneficiary, and name of the remitter. The payment order must be authenticated with the authorized signatures of the remitting bank. Chapter3. Remittance.")

225

Usually adopted procedures for M/T and T/T

(4)Upon receipt of the payment order, the paying bank verifies the authorized signatures notifies the beneficiary,and pays to him the stated amount minus expenses charged by itself. (5)The paying bank claims reimbursement from the remitting bank in accordance with the latter’s instructions. The whole procedure virtually is done by entries over banking accounts, where the buyer’s bank (remitting bank) debits his account and credits the account of the correspondent bank, receipt of the payment instructions, the latter (the paying bank) passes a reciprocal entry over it account with the remitting bank and pays the money over to the exporter. Chapter3. Remittance

Upon receipt of the payment order, the paying bank verifies the authorized signatures notifies the beneficiary,and pays to him the stated amount minus expenses charged by itself. (5)The paying bank claims reimbursement from the remitting bank in accordance with the latter’s instructions. The whole procedure virtually is done by entries over banking accounts, where the buyer’s bank (remitting bank) debits his account and credits the account of the correspondent bank, receipt of the payment instructions, the latter (the paying bank) passes a reciprocal entry over it account with the remitting bank and pays the money over to the exporter. Chapter3. Remittance.")

226

汇 出 行 的 处 理 1.审核汇款 申请书 2.审核外汇管理 规定中的文件 3.收取汇款 4.计收汇费和邮电费

汇款方式:电汇(T/T)、信汇(M/T)、票汇(D/D) 汇出货币及金额大小写 1.审核汇款 申请书 收款人全称和详细地址 收款人银行(汇入行)及收款人账号 汇 出 行 的 处 理 附言:进口合同号码、款项用途 国外银行费用由何方负担、授权银行借记汇款人账户 正本合同 国际收支申报表 2.审核外汇管理 规定中的文件 发票 贸易进口付汇核销单 进口/出口货物报关单 进口付汇备案表 运输单据、保险单据 汇款有效凭证 外汇现汇 3.收取汇款 外汇现钞 4.计收汇费和邮电费 支票

、信汇(M/T)、票汇(D/D) 汇出货币及金额大小写. 1.审核汇款. 申请书. 收款人全称和详细地址. 收款人银行(汇入行)及收款人账号. 汇. 出. 行. 的. 处. 理. 附言:进口合同号码、款项用途. 国外银行费用由何方负担、授权银行借记汇款人账户. 正本合同. 国际收支申报表. 2.审核外汇管理. 规定中的文件. 发票. 贸易进口付汇核销单. 进口/出口货物报关单. 进口付汇备案表. 运输单据、保险单据. 汇款有效凭证. 外汇现汇. 3.收取汇款. 外汇现钞. 4.计收汇费和邮电费. 支票.")

227

密押 1.核对汇款指示、汇票的真实性 印鉴 汇 入 2. 审核汇款指示内容 行 的 处 理 3.检查汇款头寸,

坚持“收妥头寸、解付汇款”的原则 4. 处理汇款的退汇与查询 Chapter3. Remittance

228

SWIFTMT100格式 15 Test key密押 20 Transaction reference number(TRN)业务备查号

Value date, currency code, amount起息日,付款货币金额 50 Ordering customer汇款人 52X Ordering bank汇出行 53S Sender’s correspondent bank 汇出行之代理行 54S Receiver’s correspondent bank汇入行之代理行 57S Account with bank受益人之账户行 59 Beneficiary customer受益人 70 Details of payment汇款用途 71A Details of charges费用支付情况 72 Bank to bank information汇出行与汇入行间业务指示

229

汇款头寸的拨付 一、汇出、入行之间建立了往来账户关系 二、汇出、入行在同一第三方银行(碰头行)开立账户 三、汇出、入行在不同的银行开立账户